Since March of 2022, the war between Russia and Ukraine has significantly impacted the global economy, affecting recovery from the COVID-19 pandemic and reducing or halting growth in most of the world’s regions. By disrupting the supply of agricultural and energy commodities, it has also fuelled inflation, which was already running hot before the war broke out.

Latin American and Caribbean countries have not been spared. The IDB’s 2022 Macroeconomic Report, released in April, looked at the war’s potential impact on the region’s exports, trade and current account balances for 2022. It warned that countries where the current account balance was deteriorating would have to seek additional external financing amid adverse conditions. It correctly anticipated that the central banks of developed economies would continue increasing their benchmark rates and continue mopping up liquidity to fight domestic inflation.

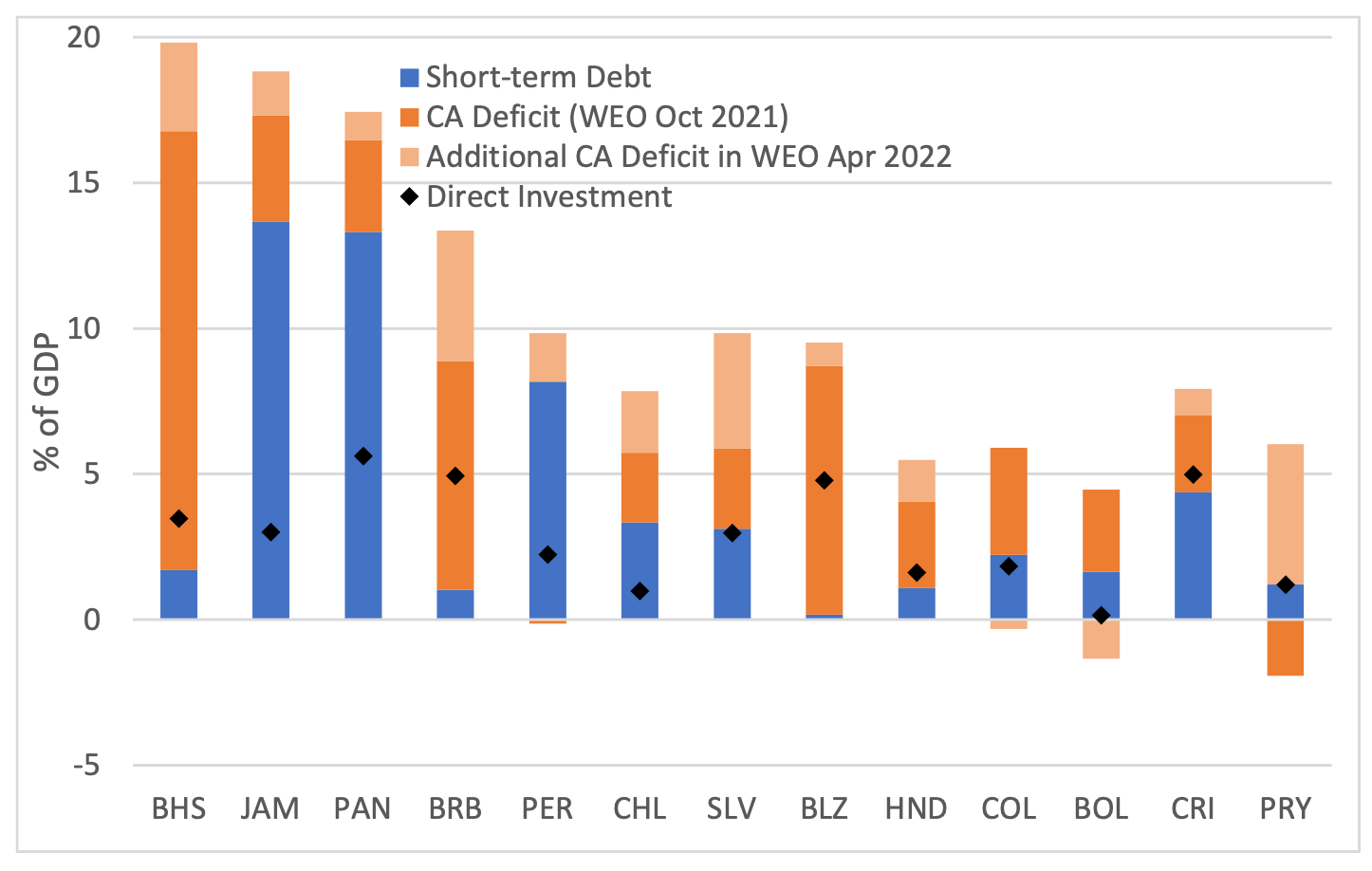

It is not surprising, given this context, that most countries in the region have faced greater external financing needs. These consist of each economy’s current account (CA) deficit plus their external debt payments (amortizations). Figure 1 shows the projected external financing needs of countries in the region in which the gap between those needs and foreign direct investment (FDI) in 2022 is higher than the region’s median. Subtracting FDI makes sense: It is a stable form of financing, more related to the structural conditions of each economy and shows very little response to macroeconomic policies in the short-term.

Figure 1. The Region’s Economies with Above Median External Sector Financing Needs in 2022.

Note: Short-term debt is foreign public and private debt due in the next 12 months. We exhibit the top half of the countries ranked by their financing needs net of expected foreign direct investment inflows.

The war’s effect on external financing needs has two components. First there is a price effect because obtaining the capital required before the war is now more costly as a result of the rise in global interest rates and stagflation fears in developed economies. Second, there is a quantity effect, as the war forces countries to borrow more resources from external sources. This is almost entirely reflected in the change in the expected CA deficit, as external debt amortizations are defined beforehand.

Figure 2 presents the change in the expected 2022 current account balances between October 2021 and April 2022, according to the IMF’s World Economic Outlook’s (WEO) forecasts for the selected countries in Figure 1. While it is very likely that there were other shocks to each economy, the shock from the war generated the biggest change in the macroeconomic outlook for most of the region’s economies during that period.

An examination of the change in expected types of financial account (FA) flows shows how countries can be expected to react to higher interest rates and additional financing needs. Four categories comprise the FA flows: foreign direct investment (FDI), portfolio investment, financial derivatives, and other investment (OI), which consists of bank loans and deposits as well as multilateral and official lending and borrowing. Figure 2 also shows the change in the WEO’s 2022 forecast for these components and in foreign reserves accumulation between October 2021 and April 2022

Figure 2 groups countries according to their main source of expected additional financing to cover their greater CA deficit. The first group consists of five economies: Chile, Peru, Jamaica, Panama, and Colombia. These will rely mostly on external portfolio investment flows, which consist principally of bond issuances in international financial markets. The fact that they are able and willing to rely on portfolio investment indicates they can access international capital markets at reasonable rates because of their financial insertion into those markets, their macroeconomic outlook, and fiscal stability.

Figure 2. Change in External Flows (WEO Forecast for 2022 in Selected Countries)

Note: The figure exhibits the difference in the 2022 forecast for each flow from between the WEO April 2022 and WEO October 2021, divided by the GDP forecast from WEO Apr 2022 It shows only the top half of the countries ranked by their financing needs net of expected foreign direct investment inflows. Country groups depend on the main source of additional financing expected to cover the additional CA deficit (Portfolio Investment, Other Investment, or Reserves).

The second group in Figure 2 comprises Paraguay, El Salvador, Honduras, Costa Rica, and Belize. These economies will rely mostly on an increase in Other Investment flows (OI) to finance their additional CA deficits. The exception is Costa Rica. There the change in FDI flows is enough to fund the additional CA deficit and the additional OI inflow will compensate an expected outflow in portfolio investment. This type of external financing rebalancing is a likely consequence of the pricing effect of the war: Countries are expected to shift from sovereign bond issuances (counted as portfolio investment flows) to multilateral financing (counted as other investment flows), given that the latter has lower interest rates. Countries in this group will also likely use multilateral financing to fund their additional CA deficits. A recent study shows how access to international capital markets and multilateral lending were critical to preventing abrupt corrections in the current account during the COVID-19 crisis.

The third group in Figure 2 includes countries that are expected to use their foreign reserves to deal with the war’s impact on their external accounts: Barbados, The Bahamas, and Bolivia. Reserves are a buffer that allows countries to smoothly adjust to new external conditions. However, as shown in this study, they are also critical for countries as they seek to gain access to markets for international financing and prevent sharp current account corrections.

The conflict between Russia and Ukraine affected the external financing needs of the economies in the region, making them, in several cases, larger and more expensive. As global interest rates continue to climb and commodity prices remain high, it will be critical for economies in Latin America and the Caribbean to cleverly use their financing options to weather the storm.

Leave a Reply