The COVID-19 pandemic has had a negative impact on Barbadians and has highlighted important traits about financial vulnerability and resilience. The restrictions in movement across and within national borders in response to the public health crisis have struck a hard blow to economic activity in Barbados. Because Barbados’s economy is small and based on tourism, this has translated into a severe income shock on households. To quantify this severity, the IDB conducted a nationally representative telephone survey between May and June 2020 that shed light on the socioeconomic challenges faced by Barbadian households (full results can be found here and full microdata can be downloaded here). In this blog, we summarize its three main findings:

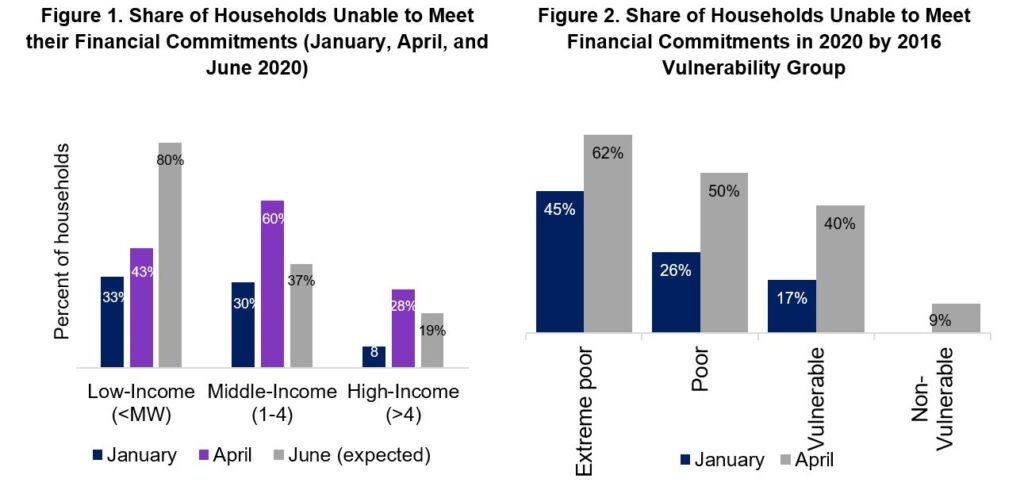

1. The relatively more disadvantaged sectors of the population have experienced the greatest increase in financial vulnerability. Widespread job losses, reduced working hours, unpaid leave, business closures, and declining remittances were highlighted as significant channels of income loss for households during the pandemic. This has led to an overall increase in financial vulnerability, measured in terms of the ability to meet financial commitments. Households with total income between 1 and 4 minimum wages before the pandemic reported the hardest short-run shock. Among this segment, the share of households that could not meet their financial commitments increased from 30 percent in January 2020 to 60 percent in April 2020. However, this group also expected their capacity to repay to improve, with a projected reduction in households unable to meet their financial commitments to 37 percent by June 2020. Similarly, low-income households (those with total income below the minimum wage) also experienced greater difficulty in meeting financial commitments in April 2020 compared to January 2020. Furthermore, they also expected their capacity to meet financial commitments to worsen in June 2020 (see Figure 1). Figure 2 shows households’ capacity to meet their financial commitments based on pre-existing vulnerability. The 2016/17 Barbados Survey on Living Conditions classified households on the basis of consumption as extremely poor, poor, vulnerable, and non-vulnerable. Although extremely poor and poor households reported the highest share of inability to meet financial commitments during the 2020 pandemic crisis, vulnerable households (i.e. with consumption levels above the poverty line but below 1.25 times the poverty line) experienced the largest relative shock (a 135 percent increase in the share of households unable to meet financial commitments between January and April 2020).

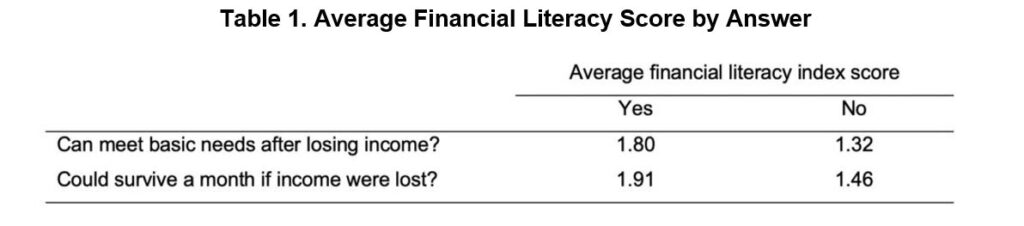

2. Financial literacy is correlated with higher financial resilience. The survey found a correlation between financial literacy and ability to withstand hardship. People who could continue to meet their basic needs during the pandemic had an average score on the financial literacy index of 1.8, compared to 1.32 for those who could not meet their basic needs. Respondents with higher financial literacy also reported a greater capacity to endure the shock. Respondents indicating that they could meet their basic needs for at least a month, in the hypothetical case that they lost their main source of income, scored 1.91 on the financial literacy index, compared to 1.46 scored by those who stated they would not be able to cope.

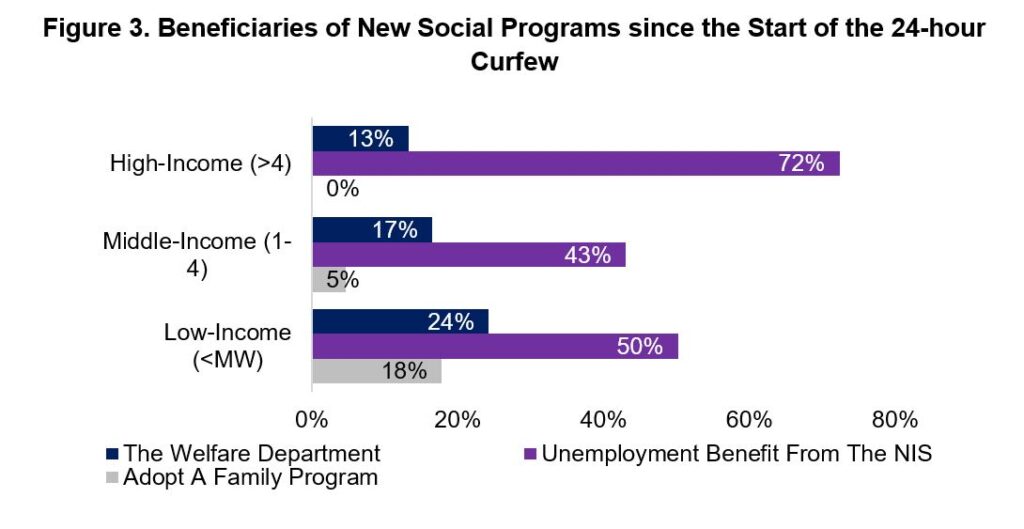

3. Social support has been a key financial resource to support households during the pandemic. The authorities swiftly increased the number and scope of social protection schemes to support the population during the COVID-19 crisis. As seen in Figure 3, social protection programs and support mechanisms provided an important source of financial support for households. At the start of the 24-hour curfew, the formal sector was heavily reliant on the unemployment benefit scheme. This support was relatively more prevalent among households with total incomes that exceeded 4 minimum wages before the pandemic (labeled as high-income). The scheme supported 72 percent of high-income households, 43 percent of middle-income households, and 50 percent low-income households. Targeted social assistance programs, namely the increased benefits channelled through the Welfare Department and the newly created Adopt a Family program, provided comparatively higher support to low-income households. Therefore, targeting of social assistance has been relatively effective.

In summary, the COVID-19 crisis has been a major shock to households in Barbados and has highlighted important trends in financial vulnerability and resilience. The key imperatives for policymakers going forward are to (i)bridge the gap by implementing continuous support measures for businesses and job protection, (ii) promote greater financial literacy for all households to improve financial resilience across all income levels, and (iii) understand how to strengthen and improve social assistance programs to facilitate efficient and sustainable support to Barbadian citizens. Full results can be found here and full microdata can be downloaded here.

Leave a Reply