With inflation in Latin America and the Caribbean running at its hottest in two decades, the issue of where that inflation comes from and what the region’s central banks might do differently has taken on great urgency.

Our newly released study arrives at a hugely important conclusion: the overwhelming bulk of inflation in the region today comes not from factors that are particular to the region, but from factors that are broadly shared globally, including post-pandemic supply chain disruptions and soaring commodity prices caused by the Russian invasion of Ukraine. Most inflation, in other words, is imported, due not to regional idiosyncrasies but to external factors.

Central banks in the region have moved very quickly and aggressively over the last year to implement the highest interest rate hikes in a quarter century to combat the inflation threat. But a big challenge remains in ensuring that households and firms have a realistic version of where inflation is headed and that they don’t unnecessarily set off an inflationary spiral with panicked visions of price increases. Effective communication from central banks to the public about where inflation is headed is absolutely essential in that regard to keeping inflation expectations grounded, or anchored.

Understanding the Globally Shared Aspects of Inflation

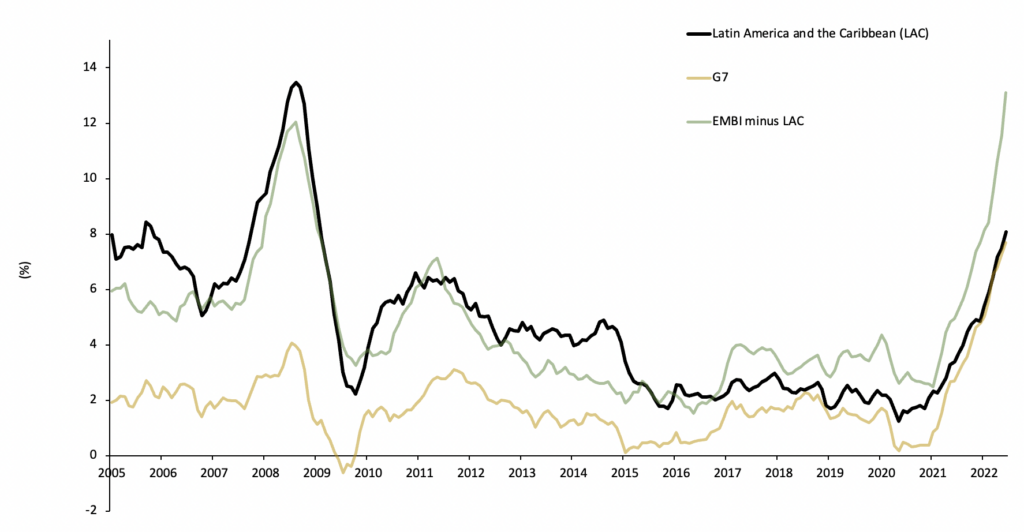

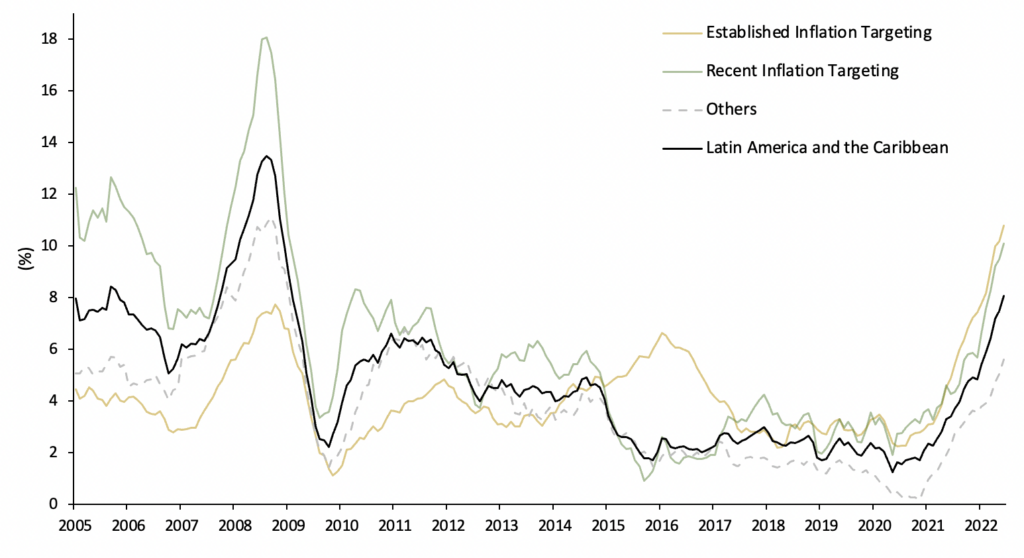

Our study analyzed a large data set encompassing inflation figures from 2005 to July 2022 from around the world, including those from the region, from 26 emerging economies outside of it and from seven advanced economies (see Figure 1). We found that up to 2020, about 60% of the variations in inflation in the region shared common factors with those from other parts of the world. After March 2020 when the pandemic struck through to the middle of this year – the last point of our analysis, the effect of these common factors significantly intensified. Today, a full 84% of the variations in inflation in the region can be explained by factors that are broadly common worldwide. Moreover, this is true for monetary regimes in the region that are highly diverse, including those that are dollarized, those that use fixed exchange rates, and those that implement inflation targeting (see Figure 2)

That is not the whole story, of course. In some countries, a growing share of inflation can now be explained by its internal dynamics, some associated with excess demand stemming from government efforts to contain the impact of prices, and others with indexation and inflation pass-through issues. Still the role of external, common factors is huge.

The conundrum for central banks in the region, as for many outside it, is how high to keep interest rates to effectively battle inflation, without provoking economic instability or a deep economic downturn. So far, the policy response in the region has been largely successful. Given the extremely large extent of imported inflation, however, one of the most important responses will lie in keeping inflation expectations anchored, thus reducing the cost of financing and making portfolio investments in government bonds more attractive.

What Central Banks Can Do

Effective communication in terms of keeping not only professional forecasters but also households and firms well-informed about where inflation is coming from and what the central bank is doing about it is absolutely essential in this regard. That could involve everything from meeting with business chambers and managers of important industries to using social networks and TV ads to announce and explain inflation targets to the general public. Such measures are key to helping households make informed decisions about their spending and saving, and allowing firms to make wise decisions about investments and hiring. They are fundamental to maintaining central bank credibility and keeping the inflation expectations in line with central bank targets. This is crucial, particularly in times of salary negotiations, when imbedded mechanisms to perpetuate inflation arise.

As our study shows, high-levels of inflation are a universal phenomenon determined by outsized, external factors like the aftershocks of the pandemic and the Russian invasion of Ukraine. Armed with that information, central banks can take more informed decisions and do the essential work to ensure that inflation expectations remain anchored.

Figure 1. Latin America and the Caribbean’ inflation shares a principal component with the rest of the world

Notes: The principal component for Latin America and the Caribbean includes: Bahamas,

Brazil, Bolivia, Chile, Colombia, Costa Rica, the Dominican Republic, Ecuador, El Salvador, Guatemala, Guyana, Honduras, Jamaica, Mexico, Panama, Paraguay, Peru, Trinidad and Tobago, and Uruguay. The principal component for EMBI countries excluding Latin America and the Caribbean corresponds to: Armenia, China, Cote d’Ivoire, Croatia, Egypt, Georgia, Hungary, India, Indonesia, Kenya, Latvia, Lithuania, Malaysia, Namibia, Nigeria, Oman. Pakistan, Philippines, Poland, Romania, Russia, Senegal, Slovakia, South Africa, Tunisia, and Zambia. The advanced economies groups (G7) is composed by Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.

Figure 2. The increase in the principal component across monetary regimes

Leave a Reply