During the COVID-19 pandemic, governments in Latin America and the Caribbean spent generously to support families, firms and banks, helping to ease the economic pain but also pushing public debt well above historic levels. Those levels of debt, which stood at 72% of GDP across the region in 2020, create substantial strain on countries in the region. Some see their currency depreciating, and with borrowing costs rising due to higher global interest rates, debt servicing has become ever more burdensome.

What is Fiscal Fatigue?

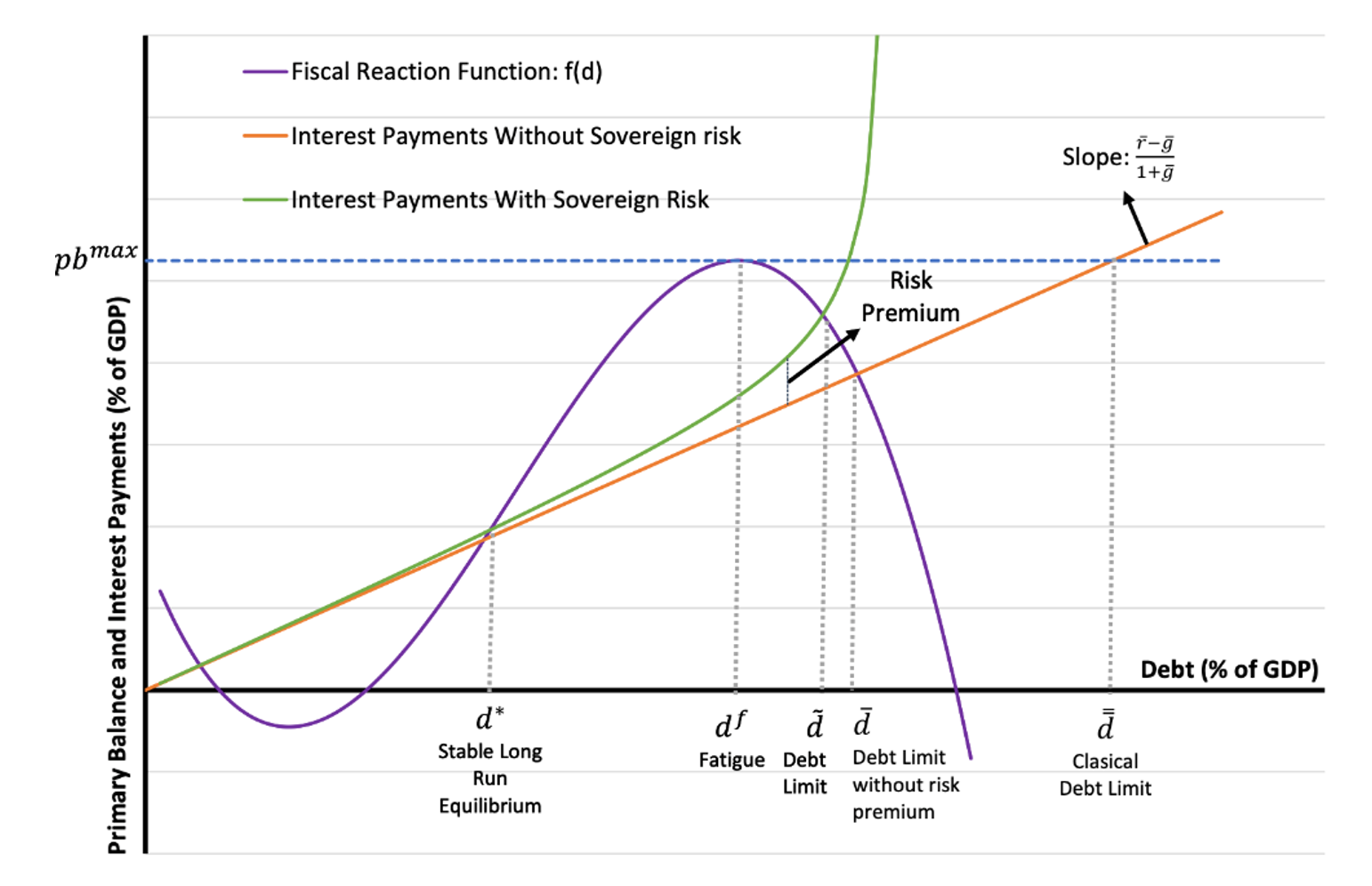

Fiscal fatigue refers to the point where a government’s primary balance — the fiscal balance minus interest payments on their debt — can no longer respond adequately to escalating levels of debt. It is, in other words, the point where governments can’t increase their revenues or reduce spending as swiftly as their debt escalates.

Figure 1. Fiscal Reaction Function

This situation, of rising public debt together with an insufficient primary balance, is potentially detrimental to economies. It means governments may have to finance their requirements at higher costs due to inflated interest rates or risk default by failing to fulfill their obligations. It creates vulnerabilities and places countries at risk of entering into financial crises.

Fiscal fatigue can be visually depicted by charting the relationship between the primary balance and debt—a relationship encapsulated in a fiscal reaction function (FRF). In Figure 1, fiscal fatigue starts to appear when the slope of the FRF starts to decrease and becomes critical at the point where the primary balance reaches its maximum value. Beyond this level, the primary balance can’t keep pace with the rising debt, leaving governments unable to meet their financial obligations.

Is There Fiscal Fatigue in the Region?

Several empirical methods have recently been developed to assess debt sustainability and fiscal fatigue. One popular method is to estimate the “slope” of the Fiscal Reaction Function (FRF), that is to use econometric (statistical) techniques to determine how the current primary balance responds to the public debt level from the previous period. The slope here is the marginal effect of debt on the primary balance—how the primary balance alters when there’s a one-unit increase in the debt-to-GDP level.

Estimating fiscal fatigue, however, isn’t straightforward. The most common FRF specification assumes that the primary balance’s response to changes in debt is always the same. But to assess fiscal fatigue, it must have the chance to vary at different debt levels. To counter this limitation, we can examine whether the primary balance’s marginal response diminishes as debt increases, indicating impending fiscal fatigue. By comparing the marginal response when debt is above and below the median, we can see if the primary balance’s response weakens (indicative of fiscal fatigue) when debt is high (exceeds the median).

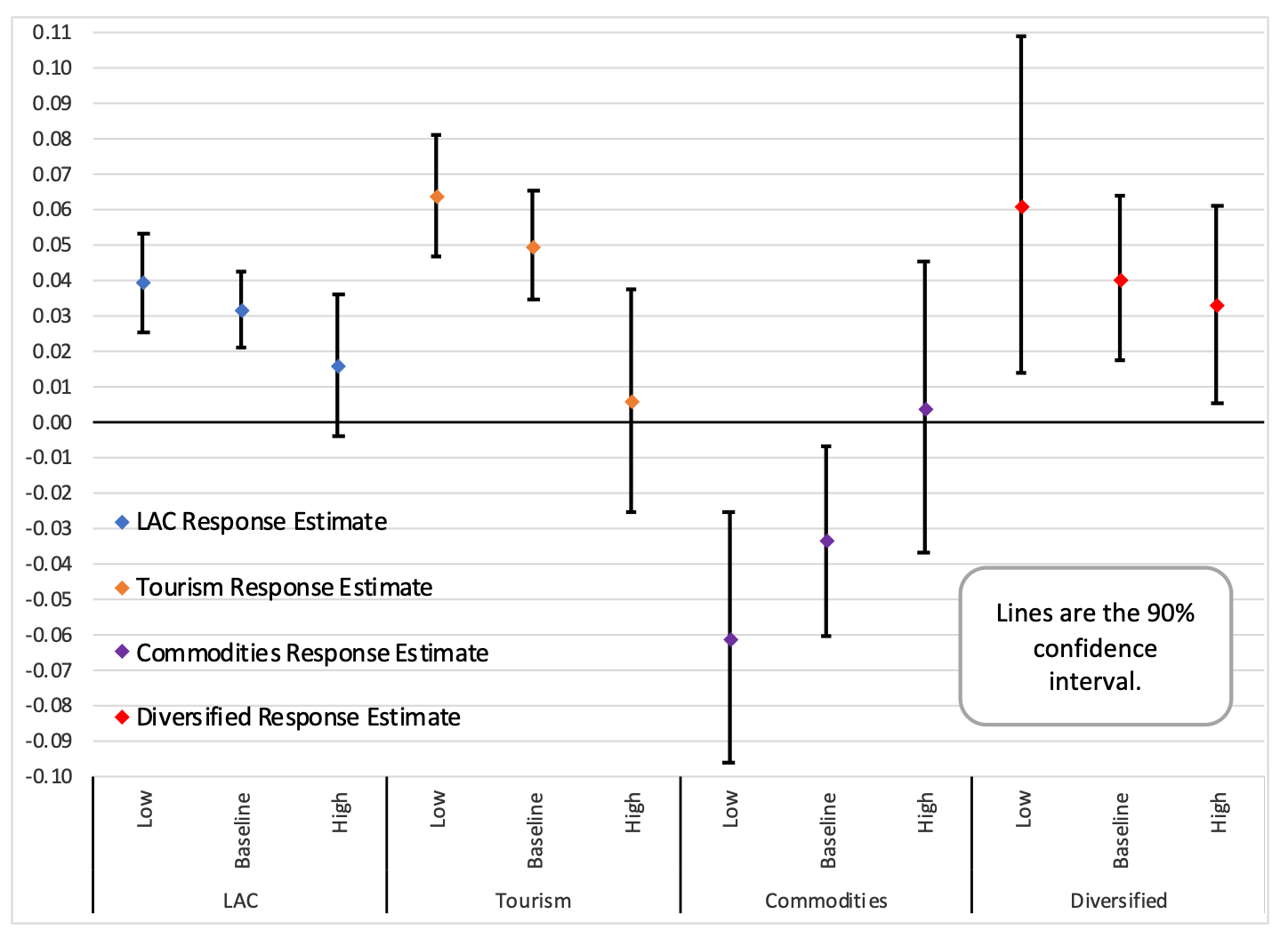

Figure 2. Primary Balance Response to 1% Increase in Debt for Economies in Latin America and the Caribbean

In a recent study, we employed this approach to gauge fiscal fatigue in Latin America and the Caribbean. Given public debt-to-GDP ratios in the region, we see how fiscal fatigue has become an emerging reality. Our FRF slope estimates suggest that, at the regional level, the primary balance becomes less responsive when debt surpasses its median.

We further split the region’s countries according to their main export: Tourism, commodities, or diversified (those countries whose main export is neither tourism nor commodities). This pools together countries facing the same external shocks, like changes in commodity prices or tourism flows, and allows for a cleaner look into how their fiscal policies react. When we estimate the slope of the FRF for each of these groups, we found some evidence of fiscal fatigue in countries that belong to the tourism and diversified groups.

The study also presents other estimates of changes in the slope of the FRF for the region as a whole and for the three groups mentioned above. These reinforce the point that at the current debt levels, the region’s primary balances react very little to debt increases.

Fiscal Recommendations

At a time of too high public debt levels, with debt pricier due to increased interest rates and depreciated exchange rates, it’s essential to design strategies that will bring debt back down to prudent levels. Policymakers can focus on creating better fiscal institutions, improving debt management, and implementing fiscal consolidation, among other approaches suggested in the IDB’s recent flagship report “Dealing with Debt.” This can help prevent unmanageable growth in debt and potential defaults and safeguard the welfare of the region’s economies.

Leave a Reply