![]()

![]() An old Irish joke has a tourist in the rural west of Ireland asking a local if he knows how to get to Dublin. After a long pause and considerable thought, the local replies, “yes, but I wouldn’t start from here.”

An old Irish joke has a tourist in the rural west of Ireland asking a local if he knows how to get to Dublin. After a long pause and considerable thought, the local replies, “yes, but I wouldn’t start from here.”

Unfortunately, with the highest overall fiscal deficit of any region of the world in 2017 (over 6% of GDP) this is a bit how it feels in Latin America and the Caribbean[1]. And like a tortuous ride to Dublin, fiscal adjustment started in 2015 and lower (primary) spending or higher revenues are expected to add an additional 2% of GDP to the fiscal balance over the next 5 years[2]. As 2017 ends, this blog reviews how the region got to this point, how deeds don’t always match the plans and what’s to be done in 2018 and beyond.

Readers of the Latin American and Caribbean Macroeconomic Report will be well aware how the region arrived to such a deficit. The aftermath of the global financial crisis, coupled with a strong rebound in commodity prices prompted many countries to pursue expansionary fiscal policy. More specifically there was a significant increase in inflexible government consumption. As argued in the IDB reports these last several years, this cannot be regarded as a counter-cyclical response. Nor was it an appropriate boost in spending reacting to a (temporary) commodity price boom. It was simply an expansion. As growth came back after the global crisis, several countries grew at rates above their potential and simultaneously maintained an inappropriate expansionary fiscal stance: deficits rose as did debt ratios. And then came the commodity bust with sharp falls in fiscal revenues, lower growth and the need for procyclical fiscal adjustment.

Gradualism has benefits and risks

Given the poorly conceived fiscal policies of the past, it is critical to get the adjustment phase right. Indeed debt positions in some countries suggest that if adjustment is also poorly designed, this may result in serious financial problems emerging. As growth is low, below potential in many cases, fiscal multipliers may be high. So, there is a prima facie case for gradualism. A tough immediate adjustment might even be counter-productive, reducing growth more than the deficit and so not reducing debt to GDP ratios at all, as well as encouraging a political backlash. But successful gradualism is not straightforward. Discounting inflationary monetary financing, gradualism means higher debts and so can only be attempted if there is room to increase debt levels and maintain sustainability. Increasing debt means greater risks, particularly vulnerability to interest rates and shifts in investor sentiment. Countries adopting a gradualist approach need to maintain a prudent debt structure and low interest rates and take measures to reduce the likelihood of a sudden stop. If the private sector does not believe in the announced plans, then it will demand higher interest rates, reducing investment and growth and increasing the probability that the access to financing will slam shut. Gradualism requires credibility and that deeds match promises. How does Latin America and the Caribbean fare in this regard?

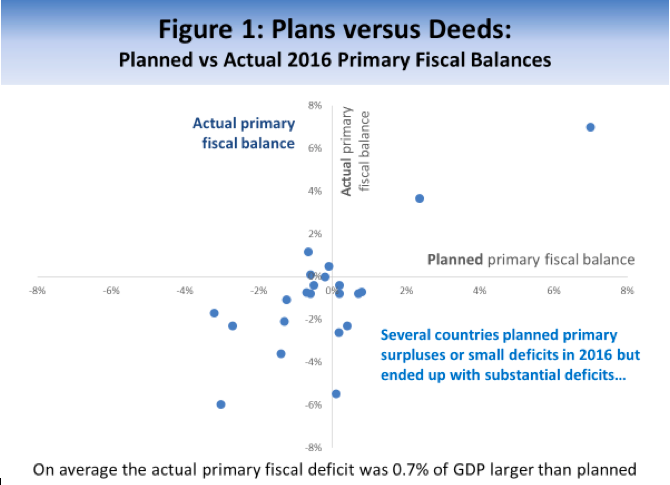

For a set of countries in the region, Figure 1 compares actual 2016 primary fiscal deficits with the plans around the end of 2015—in most cases as stated in the 2016 budget. On average, the actual deficit was about 0.7% greater than that planned and, as can be seen, a group of countries budgeted for small primary surpluses but ended up with substantial deficits. Note the exceptional case of Jamaica that announced and obtained a primary surplus of about 7% of GDP, as it has for the last 7 years, since its first debt restructuring of 2010.

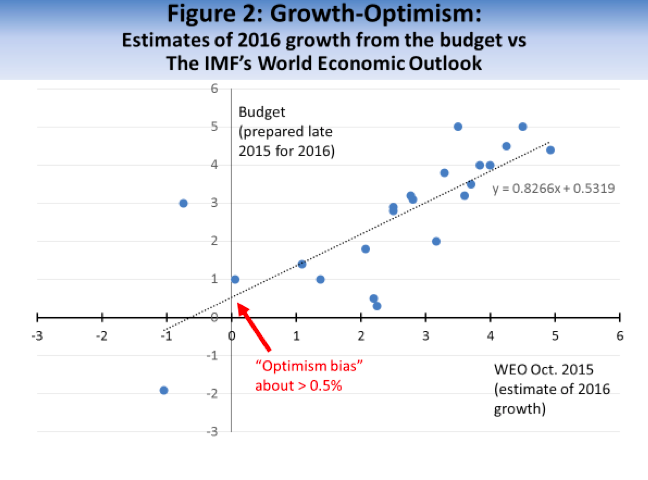

The higher than planned average deficit was not due to significantly higher spending. Rather, it seems many countries were too optimistic about growth. Comparing growth forecasts for 2016 made in budgets around the end of 2015 with the IMF’s predictions for 2016, as published in the October 2015 World Economic Outlook, the over-optimism on growth amounted to more than 0.5% — see Figure 2.

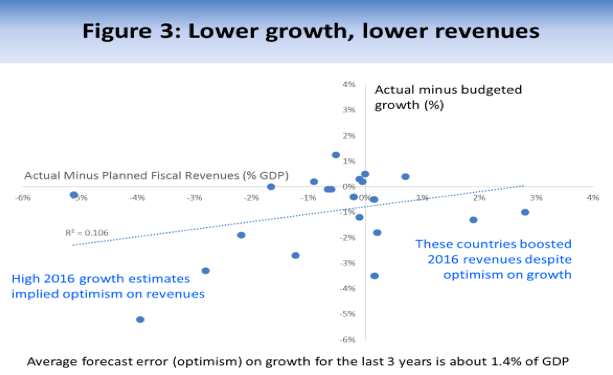

Moreover, as might be expected, growth-optimism was related to over-optimism on fiscal revenues. In other words, the lower growth was relative to the forecast, the lower fiscal revenues were relative to the amount stated in the 2016 budget. This relation is depicted in Figure 3.[3]

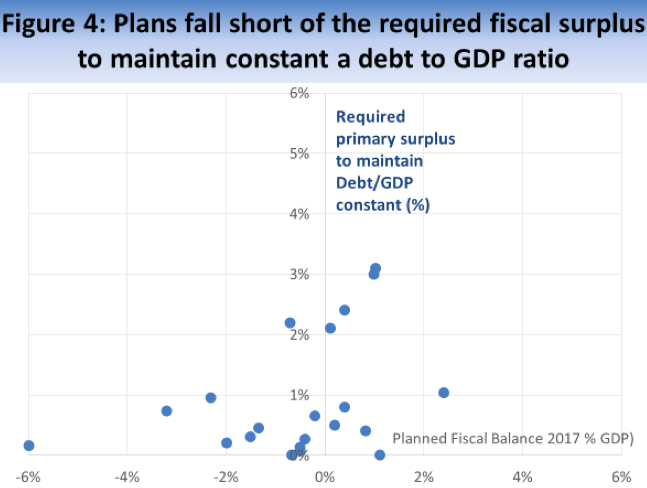

As yet, we do not know the outcomes for 2017. But most countries have budgeted for fiscal balances that will not keep debt levels constant, and, in the majority of cases, debt will continue to rise. The relation between the required fiscal surplus to maintain constant debt and the 2017 planned fiscal balance is graphed in Figure 4. All countries analyzed need a positive primary surplus to stabilize debt ratios. But many have budgeted a deficit, and for those with budgeted surpluses, several fall short of the debt-stabilizing level.

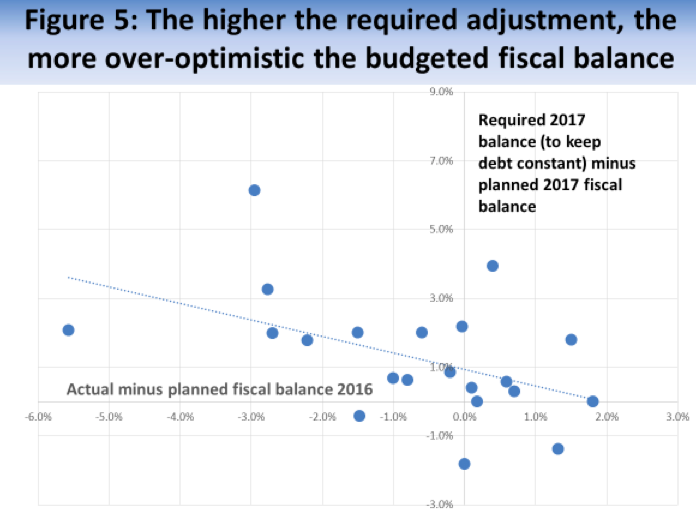

Moreover there appears to be a relation between the forecast error for the 2016 fiscal deficit and the required fiscal adjustment to keep debt constant — see Figure 5. In other words, the higher the required adjustment to keep debt constant, the more over-optimistic countries tended to be on the fiscal balance, compared to the out-turn 2016 level. This reminds me of when I was in high-school. The more difficult (or tedious) the homework, the more I would procrastinate, becoming increasingly (over) optimistic that I could finish it all the night before!

Improving efficiency and reforming tax systems

So, what needs to be done? If adjustment is required, there is a technical aspect to designing the right measures. If countries have relatively high spending levels and a high tax burden (as do many countries in South America and some in the Caribbean) raising taxes further may hurt growth. So its better to focus on rationalizing spending. Countries in Central America tend to have lower expenditures and lower taxes and increasing revenues can play a greater role. Across the whole region, there is space to improve efficiency both in terms of getting more out of each dollar of spending[4] and designing tax systems and improving tax administration to raise revenues. Tax reforms can reduce costs in terms of growth, widen the tax base and deepen automatic stabilizers[5]. Where spending is to be cut, tough choices need to be made. Cutting productive public investment may hurt growth. So it may be better to focus on streamlining government consumption, particularly on reducing subsidies or transfers that benefit the middle or even upper classes and not the poor. Estimates suggest considerable leakage from government programs to the non-poor[6]. The adjustment process in Brazil is a fascinating case in point. A pension reform to trim benefits that have increased for the non-poor is politically challenging. But if it is not achieved cuts in discretionary investment spending will be required to comply with a constitutional cap on spending. And that would hurt growth and imply greater required adjustment, higher debts and elevated risks.

Apart from the technical aspects, there is also space to improve institutions to ensure that deeds match plans and guarantee greater consistency in policymaking[7]. If a gradual approach to adjustment is adopted, then the credibility of announced plans is key. Measures such as a) publishing macroeconomic forecasts b) publishing forecasts of the main fiscal aggregates c) providing an ex-ante comparison with the forecasts of the main international financial institutions d) having an independent agency to assess performance e) developing medium-term revenue and expenditure forecasts and f) having binding multiannual restrictions on expenditures, can all play a useful role. Some countries in the region do have some of these policies in place but very few have most. As Latin America and the Caribbean continues the Big Adjustment, ensuring the right adjustment plans and greater confidence that plans will be matched by deeds will help keep interest rates low, help maintain investment and growth, and lower the interest rate costs of debt. This will minimize financing risks, and less painful adjustment will be required.

Notes

[1] Acknowledgements: I have benefitted immensely from many conversations with IDB colleagues on these topics including Martin Ardanaz, Vicente Fretes, Gustavo Garcia, Alejandro Izquierdo, Carola Pessino, Jose Juan Ruiz, Rodrigo Suescun, and Guillermo Vuletin. I also want to thank the four IDB Regional Economic Advisors, Marta Arranz, Fabiano Bastos, Osmel Manzano and Moises Schwartz, and the group of Country Economists for the underlying information regarding countries’ plans and deeds and Mariano Sosa for excellent research assistance. All mistakes remain my own.

[2] The primary deficit for LAC has fallen from 2.6% of GDP in 2015 to an expected 2.2% this year and is expected to continue to improve to a deficit of just 0.1% by 2022. Source: IMF World Economic Outlook October 2017.

[3] The slope coefficient in figures 2 and 3 are statistically significant although with such few observations I do not claim much in terms of robustness, it would interesting to extend this analysis several years backwards.

[4] The IDB’s 2018 Development in the America’s flagship for 2018 will focus on improving government spending.

[5] The lack of automatic fiscal stabilizers might be blamed for the widespread resort to discretionary fiscal policies employed in the wake of the global financial crisis although it does not necessarily account for their poor design as a potentially counter-cyclical policy response.

[6] See Latin American and Caribbean Macroeconomic Report 2015, Ch7.

[7] In this discussion I abstract from the issue of fiscal rules which was dealt with in a recent blog.

Leave a Reply