Guyana’s economy is on the verge of a historic transformation following recent oil discoveries. Financial sector development and inclusion will be crucial to maximize the benefits of faster growth and increased revenues. However, financial access and inclusion in the country are lagging, which hinders firms’ productivity and performance.

A new publication from IDB economists Victor Gauto and Henry Mooney—available here—assesses related challenges and opportunities, and provides policy recommendations for accelerating financial sector development in Guyana.

Click to listen to the podcast:

Guyana on the verge of a historic transformation…

Recent oil discoveries are expected to transform Guyana into the fastest growing economy in the world—pre-COVID-19 crisis estimates envisioned an average annual growth rate of 28 percent between 2019 and 2024. While the shock to commodity prices brought on by the crisis will undoubtedly affect these outcomes, it is still likely that Guyana’s windfall will make it one of the fastest growing economies in the world for the foreseeable future.

Why are financial access and inclusion so important?

In this context, an important objective of the government has been to develop the policies necessary to translate this newfound wealth and income into faster and more inclusive economic development. One important area is financial sector development and access. Recent research suggests strong positive linkages between financial sector depth, access to financial services, and economic development outcomes. Studies also find that financial inclusion—typically defined as the proportion of individuals and firms that use financial services—is crucially important for development and poverty reduction, and that the poor stand to benefit considerably from the use of basic payments, savings, and insurance services. Financial development and inclusion can also contribute to stronger innovation, job creation, and growth performance.

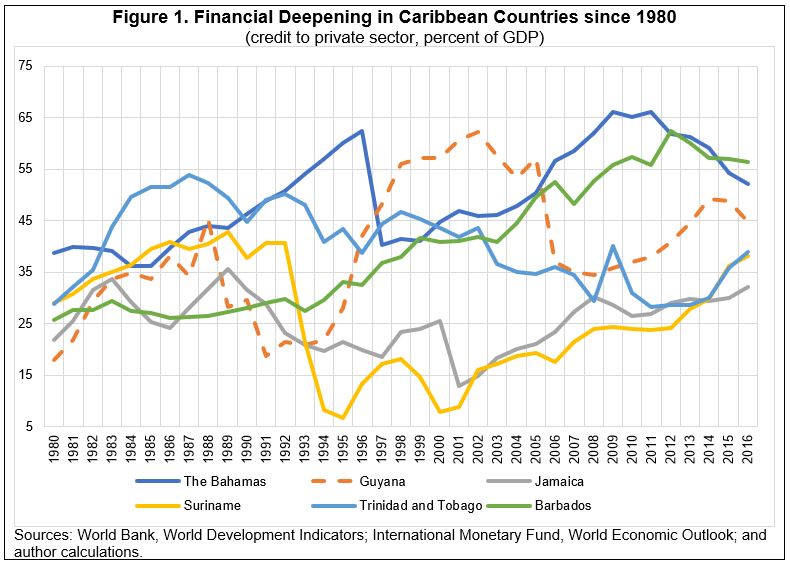

Financial Development in Guyana: Well Behind Middle-Income Peers

As a point of departure, the study considers the history of both economic and financial development in Guyana. What is clear is that the country’s history of volatile growth, debt crises, and other policy weaknesses have had an adverse impact on financial sector development. In this context, Guyana’s financial sector is relatively shallow compared to other middle-income countries—its ratio of domestic private credit to GDP was 48.9 percent in 2016, compared to 95.4 for middle-income countries across the world. While comparing relatively well with some other countries in the Caribbean region—e.g., Jamaica, Suriname, and Trinidad and Tobago—, it lags well behind others like The Bahamas and Barbados (Figure 1).

Lack of access to finance presents a challenge for firms in Guyana…

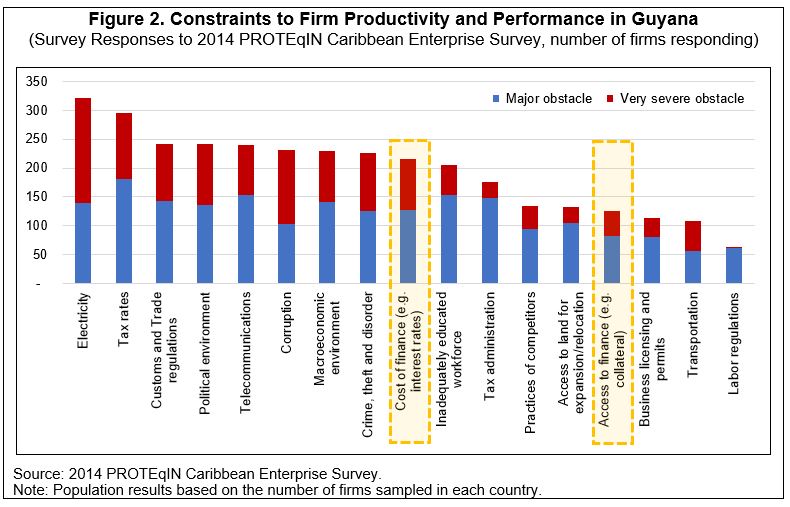

Using survey data[1], authors find that a lack of access to finance and the high costs of financial services have been identified by many firms as important constraints to private sector productivity and expansion[2] (Figure 2). Taken together, these two hurdles linked to financial development and access suggest that there is considerable scope for improvement, which will be crucial for ensuring that the newfound oil wealth supports private sector development.

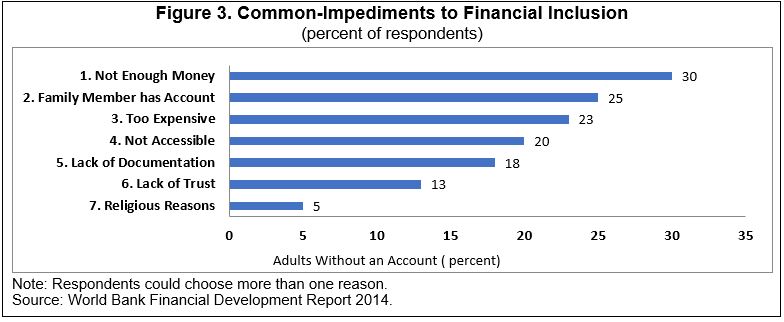

Common impediments to financial access and inclusion also affect Guyana…

After concluding that challenges are evident in Guyana, authors focus on the nature of impediments to financial development, access, and inclusion, using a number of approaches, including: (i) an assessment of the structure of the domestic financial system; (ii) data regarding the use of credit and savings products; (iii) information on the availability of financial access points relative to other similar countries; (iv) as well as an analysis of common impediments to access and inclusion based on cross-country studies and surveys (see Figure 3 for commonly-cited impediments to financial inclusion explored in the paper).

Conclusions and Recommendations

The methodologies employed and results of related exercises are detailed in the paper, and taken together, these support a number of policy relevant conclusions and recommendations:

- Development and implementation of a comprehensive financial inclusion strategy. Many countries in the region and around the world have developed comprehensive financial development and inclusion strategies, including Haiti and Jamaica in the Caribbean. These take a holistic approach to identifying policy failures, infrastructure and institutional gaps, and other country-specific barriers to access and inclusion.[3] Guyana should develop such a strategy, that would better define impediments, and act as a catalyst for progress.

- Reducing the costs of finance. The analysis suggests that banks in Guyana are quite profitable and display comparatively wide loan-to-deposit spreads, particularly when compared with regional and global peers. High interest rates may stem from several factors, including the funding structure of banks, or regulatory or supervisory issues. It may also relate to the risks inherent to borrowers and their intended uses of funds. In this context, the availability of information regarding borrower credit histories and risk profiles are relevant. While more analysis is required to properly target reforms or policies, efforts undertaken in other countries to improve the availability of credit- and risk-related information have proven helpful, as have efforts to improve the capacity of market participants to develop business plans and lending proposals.

- Encouraging competition for banking services. Strong bank profitability may be an indication of a lack of competition in the sector. In this context, authorities might consider fostering competition in the sector via regulatory or policy measures (e.g., reducing barriers to bank entry or establishment), to the extent that these would not compromise system integrity and stability. Similarly, efforts to facilitate lower-cost virtual banking services (e.g., mobile banking) could help reduce the costs and encourage new participants.

- Developing domestic financing instruments and markets. The government should diversity domestic funding practices by introducing longer-term domestic debt instruments. This would facilitate the development of private financing instruments, by creating pricing and risk benchmarks necessary to develop a domestic yield curve. Similarly, this would help market participants differentiate between funding and monetary policy actions. Finally, issuing longer-term public debt instruments would help provide investors with alternative local currency assets, facilitating asset-liability management, and potentially reducing interest rate spreads that stifle financial access and inclusion.

- Increasing physical and virtual access for customers. Given the large proportion of the population living outside urban areas, financial access could be expanded by increasing access points in under-served areas. As above, the expansion of mobile and virtual banking services could help in this regard, supported by national payment system and related reforms.

- Enhancing financial literacy. Initiatives aimed at improving financial literacy, particularly for rural or under-educated populations, would encourage the unbanked to seek out traditional and new financial services of banks and other providers. This could be accomplished through targeted information campaigns or other means of ensuring that under-served segments of the market have the information required to make better use of the system. Along with other national initiatives currently being contemplated, developing a national financial inclusion strategy would certainly help in this regard.

To also read our assessment of Barriers to Financial Access in Barbados—Key Challenges and Focal Areas for Reform click here.

To listen more of our podcasts click here.

[1] As reported in the 2014 Productivity, Technology, and Innovation Caribbean Enterprise Survey (PROTEqIN) enterprise and indicator survey, which was last updated in 2014. The methodology was designed to: 1) benchmark economies’ business and investment climates across the world; and 2) assess effects of conditions and changes in business environment constraints on firm-level productivity and performance. The project was sponsored by Compete Caribbean, which is funded by the Inter-American Development Bank (IDB), the UK’s Department for International Development (DFID), and the Government of Canada.

[2] Electricity, tax rates, customs and trade regulations, and the political environment were also identified as among the most pressing challenges.

[3] For example, see Jamaica’s recently launched Financial Inclusion Strategy, which has been developed and implemented with support from the Inter-American Development Bank. See the following for details: https://publications.iadb.org/publications/english/document/Jamaica_Financial_Development_Access_and_Inclusion_Constraints_and_Options.pdf

Leave a Reply