The mobilization of domestic financial resources is increasingly recognized as an important development challenge for countries around the world—this is also true for Barbados. Barriers to financial access act as a brake on private sector investment and growth, with adverse implications for broader economic development objectives. In order to shed light on this issue, our latest publication—“Financial Access and Inclusion: A Diagnostic for Barbados”—presents an assessment of financial market development, access, and inclusion in Barbados, identifying common and country-specific barriers, as well as relevant policy recommendations.

Financial depth in Barbados: well behind high- and middle-income country averages…

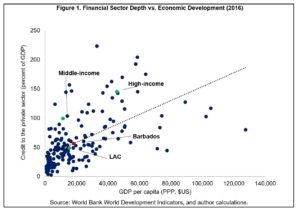

Barbados’ ratio of private sector credit to GDP is higher than many of its peers in the Caribbean, but remains low for a country at its level of income. While any assessment of financial sector development will depend on the metrics selected, the ratio of domestic private credit to GDP is generally considered a key indicator of sector depth and development.[1] Domestic credit to the private sector in Barbados stood at about 56 percent of GDP in 2016 (Figure 1).[2] This was high compared to many other Caribbean countries, but well below the average of 149 percent and 99 percent, respectively, for its high- and middle-income peers.

Financial access remains a challenge for both individuals and firms…

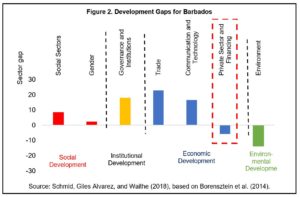

Private sector development and access to finance remain key challenges in Barbados. As highlighted in Figure 2, using Borenzstein et al.’s (2014) methodology, Schmid, Giles Álvarez, and Waithe (2018) find negative development gaps related to the private sector[3], as well as with respect to the costs and availability of financing.

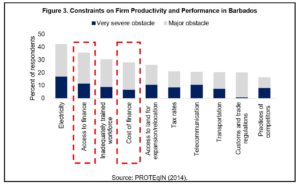

Surveys also point to important barriers linked to financial access and the costs of funding. For example, the 2014 PROTEqIN Caribbean enterprise survey also reveals that the costs of finance and access to financial services are among the most significant constraints facing Barbadian firms in terms of their productivity and performance (Figure 3).

Key Barriers to Financial Access and Opportunities for Reform

Based on metrics developed to identify common barriers to financial access and inclusion, our analysis suggests the following:

- Barbados fares well with regard to financial access for individuals. However, impediments remain regarding individuals’ ability and willingness to access financial services, linked to increasingly stringent know your customer (KYC) and documentation requirements, as well as anecdotal evidence of challenges related to financial literacy.[4]

- Firms’ access to finance is hindered by a lack of credit risk information, as well as increasingly stringent KYC and other institutional constraints. Barbados ranked 144th out of 190 countries on the World Bank’s 2019 Doing Business Report indicator for ‘getting credit’, in part reflecting the lack of a credit bureau or centralized information regarding counterparty credit risks. This contributes to burdensome collateral and other security requirements for firms—particularly for smaller ones.

Policy recommendations that stem from our analysis include:

- Continue fostering macroeconomic stability and growth, including through the pursuit of policies that support sound and stable macroeconomic performance, and private sector investment.

- Encourage the use of new technologies, while addressing regulatory hurdles. Encouraging use of new financial technologies to better incentivize and serve clients, while also revising relevant regulatory requirements to facilitate innovation and remove unwarranted documentation requirements.

- Increase the availability of information regarding credit histories and financial risks, including through the establishment of a centralized credit bureau and related infrastructure. This would help financial institutions better assess counterparty credit risks, and promote a reduction in lending costs, as well as banks’ need for additional security (e.g., collateral or guarantees). This is particularly relevant in the context of smaller enterprises.

- Develop and implement a national financial inclusion strategy. Unlike many other countries facing similar challenges across the world, Barbados has yet to develop a comprehensive financial inclusion strategy, and the policy discourse in this area has been limited to date. Such a strategy has the potential to act as a catalyst for information gathering, the identification of specific barriers across crucial sectors, as well as for the implementation of coordinated policy measures across public agencies in partnership with the private sector. Other countries—including in the Caribbean region[5]—have had tremendous success in terms of improving outcomes following the implementation of related strategies.

Click to listen more in this podcast:

For more podcasts from our Improving Lives in the Caribbean series, click here.

[1] Private credit includes funds provided to the private sector by financial corporations—e.g., loans, purchases of non-equity securities, trade credit, and other accounts receivable establishing a claim.

[2] Based on the latest available data at the time of publication.

[3] The term ‘private sector’ is based on the definition set out by in the World Bank’s ease of doing business indicators.

[4] To date, no formal assessment of financial literacy has been undertaken in Barbados.

[5] Jamaica recently implemented a comprehensive national financial inclusion strategy with support from development partners like the IDB, leading to a number of consequential policy reforms and improvements in financial access and inclusion.

Leave a Reply