Joint research from the IDB’s Caribbean Department, IDB Invest, and the Complete Caribbean Partnership uses enterprise survey data to highlight that firms from across the Caribbean face challenges when it comes to access to finance, particularly given the depth and development of credit and capital markets. Findings suggest that the most pressing barriers to finance are burdensome collateral requirements, high interest rates, complex application requirements, and an inability to find credit instruments compatible with borrowing needs. These challenges vary across countries by firm size and gender characteristics, with the most vulnerable firms generally facing the most severe challenges.

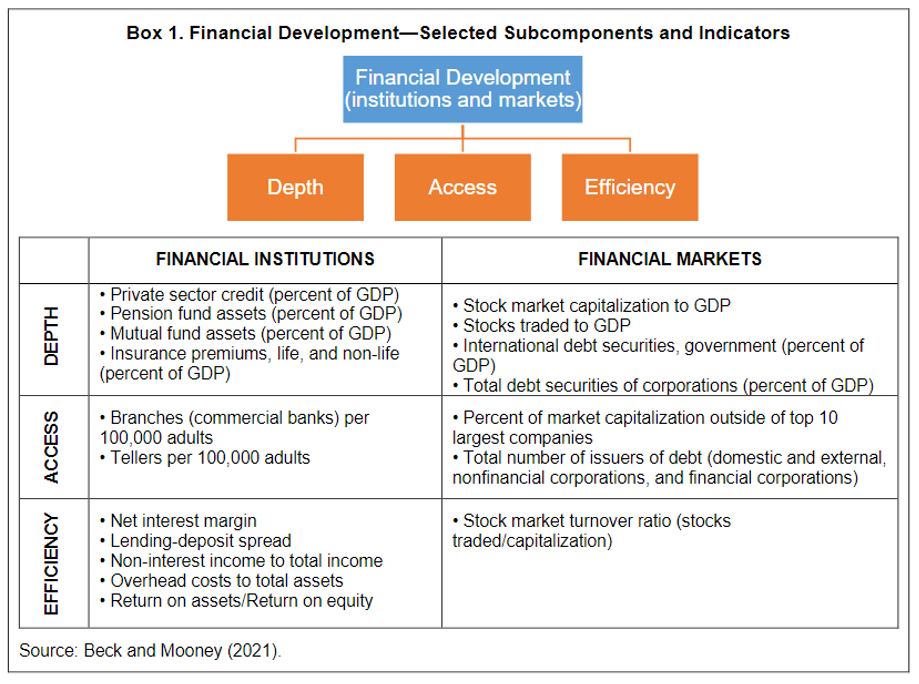

Financial development describes the extent to which financial institutions and markets can satisfy the needs of both public and private entities. Financial institutions and markets are critical to enabling transactions across space and over time, as well as pooling savings and intermediating them to enterprises and households in need of external funding. Financial development is thus crucially important for economic growth, the reduction of poverty and inequality, and other important social outcomes. Our Latest publication from the Caribbean Economics Team focuses on financial development in six Caribbean countries, with a particular focus on firms’ access to finance—one of the three pillars of financial development: depth, access, and efficiency (Box 1).

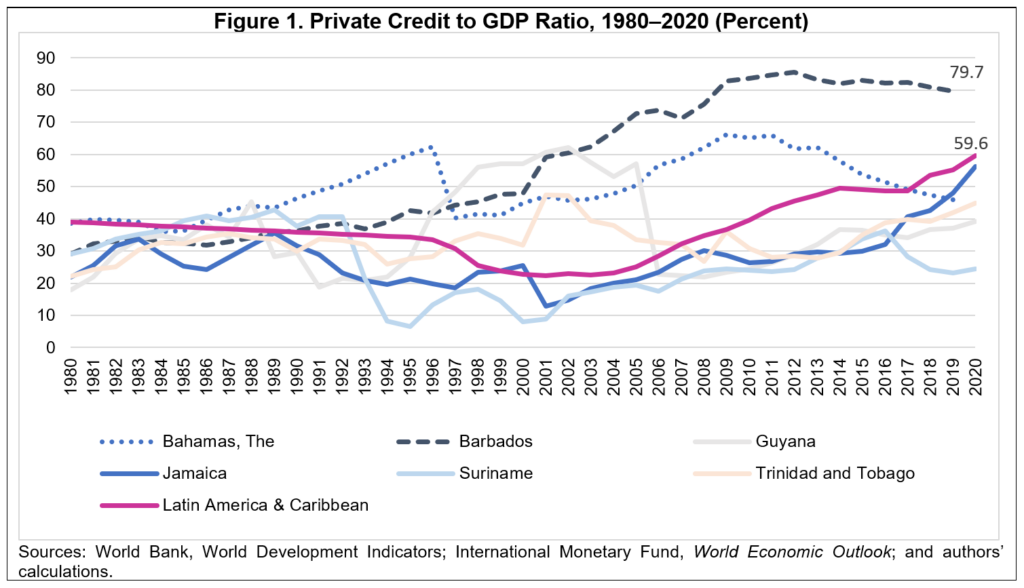

Slow Credit Growth

Over the past several decades, financial deepening in the Caribbean has been slow. While Barbados and Jamaica have seen the pace of deepening accelerate considerably, in other countries private credit has fluctuated (Figure 1) and remain well below peer country averages. Barbados has experienced considerable private credit growth (measured as a proportion of GDP) since the 2000s in line with an expansion of offshore financial services. Jamaica has also made great strides in improving its private credit to GDP ratio, from 26 percent in 2010 to 56 percent in 2020. The improvement is due to strong fiscal institutional reforms, including the establishment of fiscal rules and reforms of the public sector. For Guyana and Trinidad and Tobago, market depth has oscillated appreciably over the period owing to fluctuations in both total domestic credit to private sector and the value of domestic production. In contrast, domestic credit has been trending downwards for The Bahamas, despite hosting one of the largest offshore financial centers. In 2019, its market depth was 45.9 percent of GDP, compared to 65.1 percent of GDP in 2010. Credit market development in Suriname has remained stagnant, at an average of 27 percent of total production. Within the Latin American and Caribbean region (LAC), only Barbados outperformed the regional average with a financial depth of approximately 80 percent of GDP.

Devastating Pandemic Shock

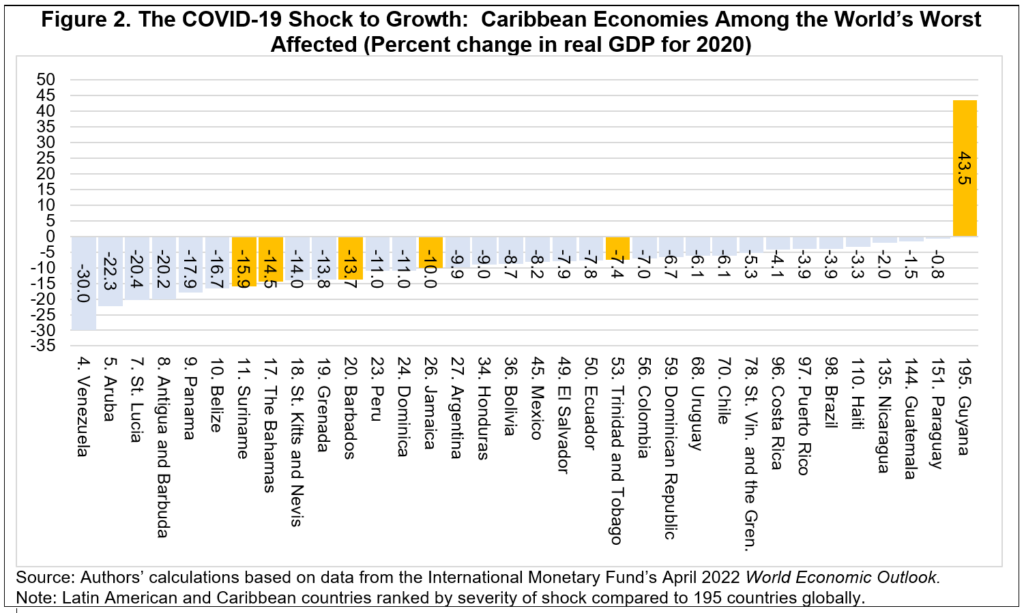

COVID-19 generated a significant economic shock for Caribbean countries. Suriname recorded the largest real GDP contraction of 16 percent, while Trinidad and Tobago saw a contraction of only 7.5 percent. These shocks would have been worse had it not been for policy actions taken by governments. As the region recovers in 2022, it is important to note that sharply rising commodity prices, driven to a large degree by the Russia-Ukraine conflict, as well as generalized inflation pressures and central bank policy responses imply a high degree of uncertainty regarding economic prospects.

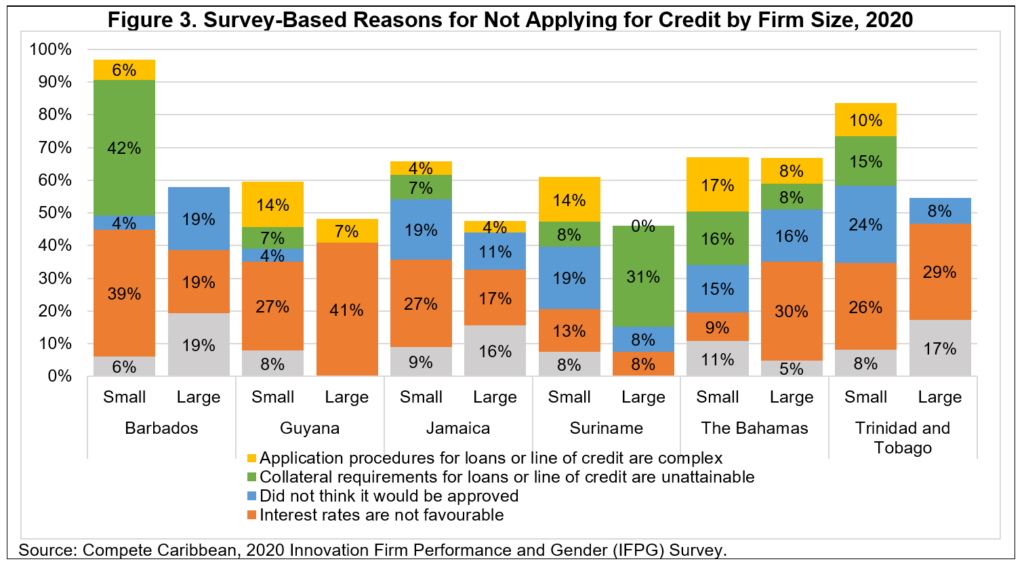

Small firms at a disadvantage

The Compete Caribbean 2020 & 2021 Innovation Firm Performance and Gender (IFPG) Survey was conducted to evaluate the private-sector environment, including the impact of the crisis. Results suggest that the most pressing barriers to finance were insufficient collateral, high interest rates, complex applications, and inadequate credit availability. Importantly, these factors varied across firm-size and, to some degree, across countries. For example, except in Suriname, small firms, which usually possess fewer valuable fixed assets, were much more likely to indicate that collateral requirements were impediments. However, large firms were much less likely to indicate that application procedures were complex, as they usually have more specialized employees in accounting and finance. As banks tightened their balance sheet while the pandemic progressed, it is likely that factors such as insufficient size and maturity of loans also worsened as firms—both large and small—sought liquidity to maintain their operations. This liquidity crunch would likely be more pronounced in tourism-dependent countries, such as The Bahamas and Jamaica.

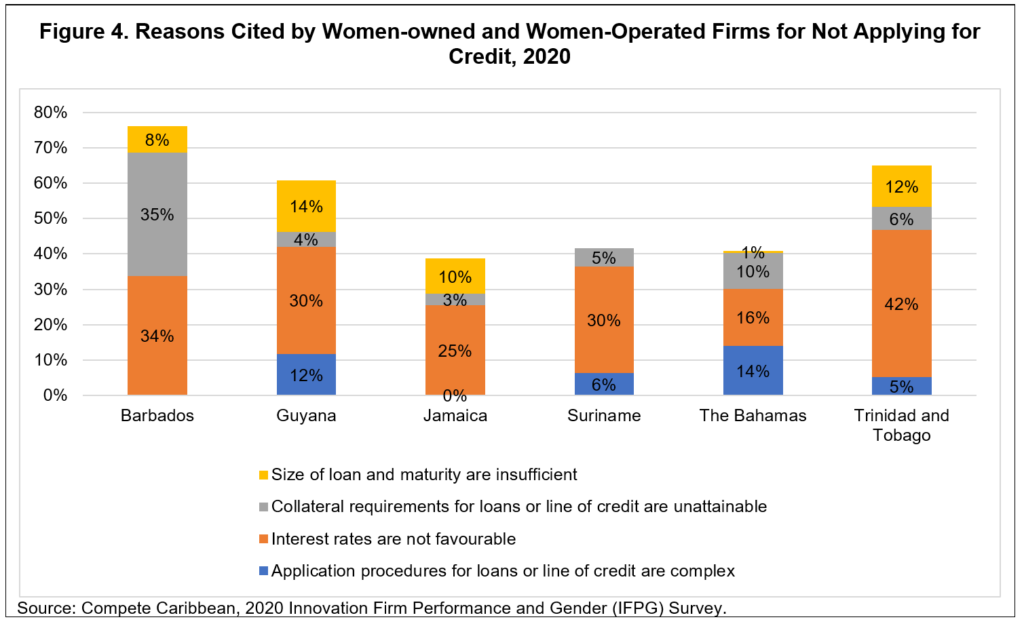

Women-owned and/or operated firms suffered most

In addition to size, gender also plays a crucial role in accessing external support, with more women-led and women-owned firms (WOFs) stating that the cost of financing is a major barrier. On average, 31 percent of WOFs indicated that high interest rates were a barrier, with WOFs from Trinidad and Tobago reporting the highest proportion (42 percent). These differences in financing challenges faced by WOFs vary across countries. For example, across the region, only 5 percent of WOFs reported that complex application procedures are a challenge in accessing credit. While no Bajan or Jamaican WOFs report complex applications as barriers, in The Bahamas, the proportion is as high as 14 percent. Therefore, the challenges that WOFs experience also vary across countries and, in some instances, are more pronounced than non-WOFs.

What can be done?

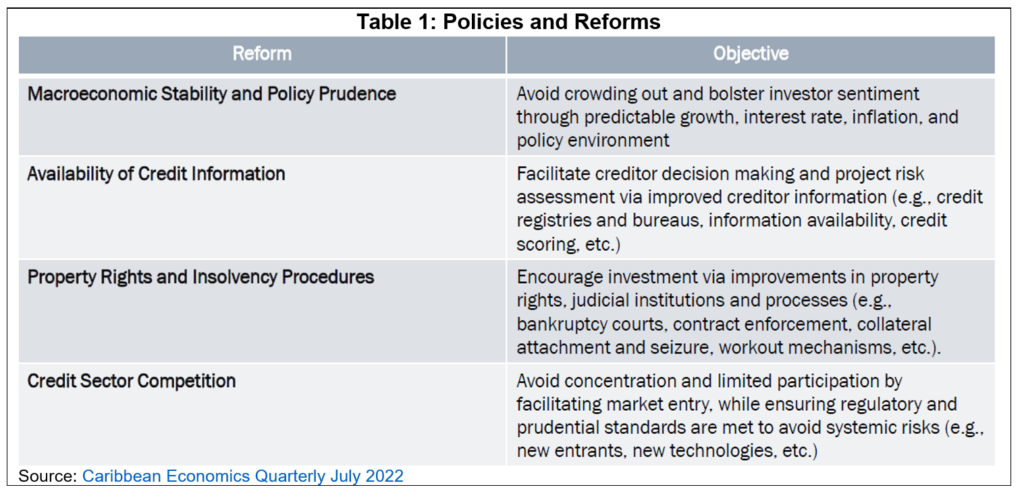

Although conditions and outcomes vary across the Caribbean, results suggest that firms everywhere are struggling to access finance. Based on our survey responses, these challenges seem to have become more acute in the last several years, in part because of the pandemic. Looking forward, there are many reforms and policy considerations that could help to advance financial development in the region (Table 1). Our report outlines many of these, including the following:

Leave a Reply