Access to adequate finance is critical to any business. For the most vulnerable – smaller firms and those owned and operated by women – finance is the lifeblood. Financing allows businesses to improve their services, expand to different markets, provide jobs in their communities, and contribute to the growth of the economy.

New joint research from the IDB’s Caribbean Department, IDB Invest, and the Complete Caribbean Partnership uses new data to highlight that firms from across the Caribbean face outsized challenges compared to other countries from around the world when it comes to firm access to finance given the depth and development of credit and capital markets.

The research finds that conditions deteriorated considerably during the COVID-19 crisis for firms across the board, and that the most vulnerable were most severely affected. The report also points to policy and market related reforms with the potential to improve outcomes, and examples of successful interventions from around the Latin American and Caribbean region that have helped to catalyze investment and support faster and more inclusive development.

Access to Finance: Key Findings

The research revealed that while Caribbean sectors are developing, the region remains behind its global peers. The COVID-19 pandemic made it harder to access financing across the region, and smaller firms face more significant hurdles than larger ones when it comes to accessing finance. Women-owned and/or operated firms face even more severe challenges than other firms across the region.

FINDING 1: Caribbean financial sectors remain underdeveloped compared to other regions.

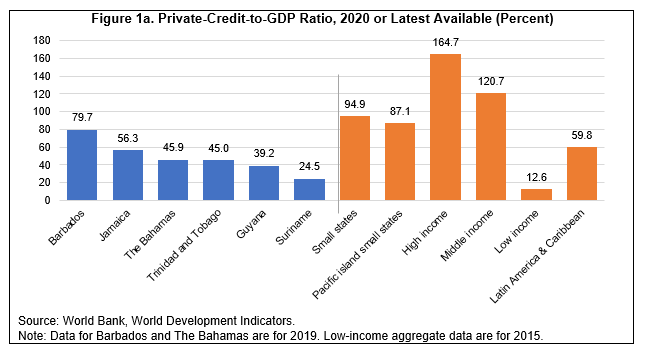

Region behind global peers. The ratio of domestic private credit to GDP—the most common indicator of sector depth—ranges from as high as about 80 percent for Barbados, to as low as about 25 percent for Suriname (Figure 1). The six Caribbean countries analyzed here compare poorly with the average for both high-income and middle-income countries, which stood at 165 percent and 121 percent, respectively (latest available). The countries also fare poorly when compared to the regional Latin American and Caribbean average. Only Barbados has a deeper financial sector than the regional average of 60 percent. Country size does not seem to be the determining factor, since the six countries are also all below the average for small states, globally, as well as Pacific Island small states.

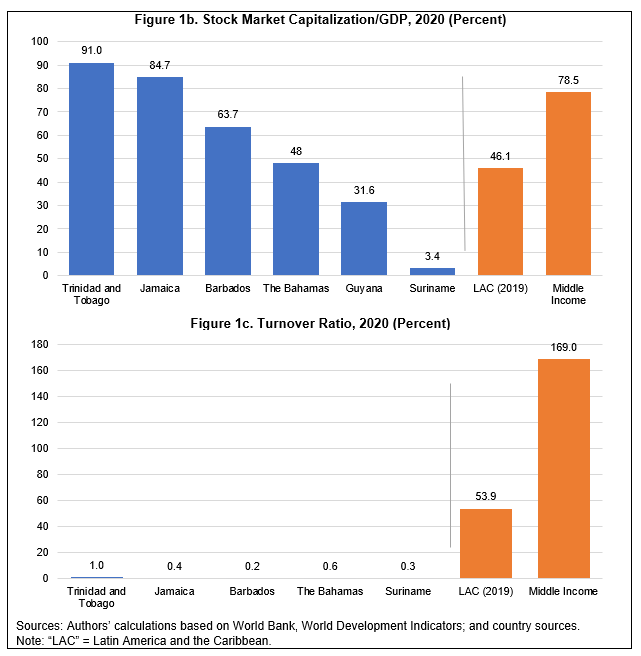

Equity markets growing, but still shallow. All six countries have stock exchanges of reasonable size relative to GDP (Figure 1b), though they are highly concentrated in terms of the number of issuing firms, and they tend to be illiquid—that is, market capitalization (value of all outstanding shares) relative to GDP tends to be relatively high, while turnover ratios (trading volumes) are very small relative to regional or middle-income country averages (Figure 1c).

FINDING 2: COVID-19 shock drove a deterioration of financial access for Caribbean firms.

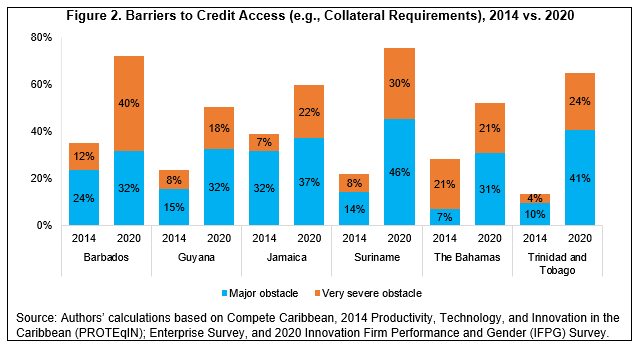

COVID-19 a severe setback. Despite a strong policy response, the Caribbean saw a considerable deterioration in financing conditions by the end of 2020. The share of firms that reported access to credit as a significant barrier to operations and activities increased between 2014 and 2020—in some cases, considerably (Figure 2). Though some COVID-related stresses have begun to dissipate, others have emerged, including rising inflation, higher domestic and external policy interest rates and their implications for funding costs, as well as increased uncertainty regarding global growth and demand.

FINDING 3. Smaller firms in the Caribbean face outsized challenges.

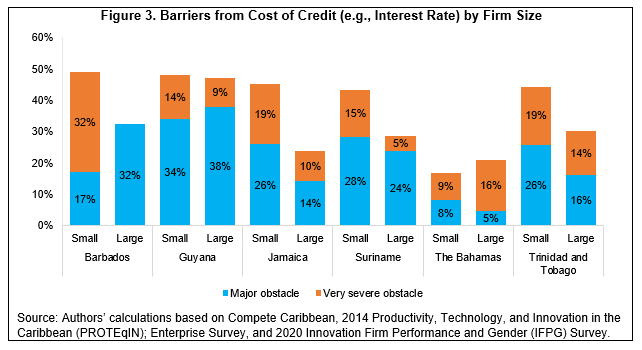

Size matters. For most countries, about half of all small firms reported financing costs as a major or very severe obstacle to operating and growing their businesses (Figure 3). In five of six countries, this was a greater proportion than for larger firms, pointing to the outsized challenges facing micro-, small-, and medium-sized enterprises across the region.

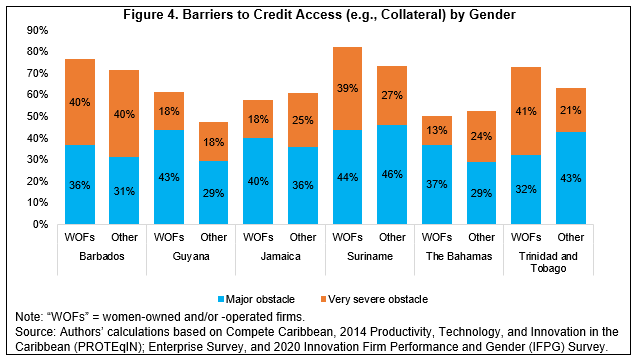

FINDING 4. Firms owned and/or operated by women face greater difficulty than others.

Women face outsized challenges. Findings also suggest that women-owned and women-led firms (WOFs) face more significant financial constraints than other firms. Between half and two-thirds of all women-owned and/or -operated firms across the six Caribbean countries reviewed report credit access (e.g., high collateral requirements) as a major or very severe obstacle to business operations. In all but one country (Jamaica), this is a higher proportion than for all other firms—in some cases, by a wide margin (Figure 4).

Reforms can improve outcomes

Concerted efforts are required to support faster financial development and broader access. These and other challenges must be overcome to support faster and more inclusive growth across the Caribbean. Efforts must include both participation of private and public sectors, as well as coordination between them and external partners. While many country-specific factors are important (also detailed in the report), several key policies and reform priorities are relevant to the region as a whole, including:

- Macroeconomic Stability and Policy Prudence: The first priority of any government wishing to create an enabling environment must be to ensure low and stable inflation, as well as fiscal prudence to avoid crowding out private credit. Similarly, policy predictability will also provide added confidence to those who would both lend and borrow, as well as invest, in local businesses and capital markets.

- Availability of Credit Information: High collateral requirements and the costs of borrowing have been reported as significant impediments to financial deepening and access. Measures such as the development of centralized credit registries and bureaus, as well as other mechanisms for risk information gathering and sharing, would support improved counterparty credit risk assessment and management. This would allow banks to reduce their need for credit enhancements (e.g., collateral and guarantees), extend maturities, and broaden the base of potential borrowers at lower costs.

- Property Rights and Insolvency Procedures: Ensuring that a country’s regulatory and judicial frameworks can provide both creditors and debtors with greater confidence in terms of property rights, contract enforcement, and the process of resolving insolvency would help accelerate financial development and improve access to credit. These are institutional areas where several Caribbean countries fall short of international benchmarks.

- Credit Sector Competition: Regulatory and other reforms aimed at stimulating healthy competition in the banking sector are important to ensure that credit can be provided at reasonable costs—one of the key hurdles identified by many firms in the region. If implemented without compromising financial stability or prudential standards, an adequate level of regulation aimed at fostering competition could encourage broader use of credit by individuals and SMEs, with benefits for all sectors of the economy.

In addition to policy and regulatory imperatives highlighted in this post, international partner institutions like the IDB, IDB Invest and IDB Lab can support efforts to create markets and financial capacity, by working with both public and private sectors to improve business planning, catalyze both external and domestic sources of funding, and enable partnerships aimed at supporting investment and business expansion. The IDB Group is committed to working with Caribbean member countries to improve access to finance for women entrepreneurs and small enterprises, which are crucial for supporting social and economic development, inclusive growth, and a better future for all citizens.

Leave a Reply