Finclusion is a combination of the words Financial Inclusion and FinTech. It is used to describe FinTech-driven financial inclusion. In this blog, we summarize the main findings of our paper on Financial Inclusion and FinTech in Suriname.

What is financial inclusion?

Financial inclusion means that individuals and businesses have access to financial products and services that are useful, affordable, of adequate quality and convenient. This includes products and services such as transacting, making payments, savings, credit, and insurance. For financial inclusion to truly exist, these products and services must be made available in a responsible and sustainable manner.

Why is financial inclusion important?

Universal financial access and inclusion are of paramount and growing importance as a means of alleviating poverty and achieving higher, sustained, and inclusive economic growth among other outcomes. In fact, the United Nations identified financial inclusion as a key enabler for achieving eight of the 17 sustainable development goals.

Financial inclusion in Suriname

In Suriname, around 32 percent of the population over the age of 18 do not hold a bank account—according to data from the Surinamese Bankers Association (SBV)(Frangie 2019). Citing FinaBank Market Research, the SBV points to the following reasons for financial exclusion: (i) No permanent job (44.3 percent); (ii) No proof of employment and or payslip (18.7 percent); (iii) No confidence in the banking system (2.4 percent); and (iv) Unfamiliar with the benefits of banking (6.5 percent).

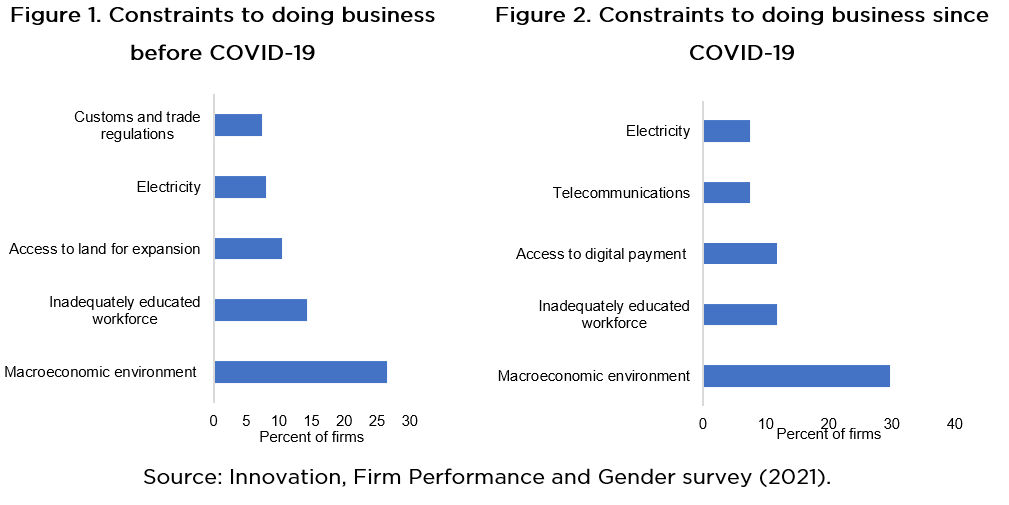

Access to financial services is also a challenge for businesses. 25.9 percent of firms in Suriname cited ‘access to finance’ as their most significant obstacle in the 2018 World Bank Enterprise Surveys (in 2010 this was 15.9 percent). Moreover, the 2021 Innovation, Firm Performance and Gender (IFPG) survey found that access to digital payment systems became a major constraint to doing business in Suriname during the pandemic (see Figures 1 and 2).

Finclusion and its benefits

FinTech, which combines financial services and solutions based on technologies, can enable financial inclusion because it makes financial services more accessible and often at a lower cost for both providers and consumers, focusing on the underserved individuals and communities. The pandemic highlighted the importance of FinTech as it provides alternatives that allow for safer transactions, such as cashless payments and contactless transactions.

However, the potential of FinTech encompasses much more than providing safer transactions. FinTech also promises greater economies of scope, broadening access to products such as savings, payments, and credit by reducing information irregularities for both consumers and financial service providers. By offering greater convenience, lower transaction costs, and better credit risk assessments, FinTech has the potential to increase the number of participants in financial markets and help lessen the urban-rural access inequalities. This could be of particular benefit to Suriname’s remote communities and geographically dispersed population. Furthermore, the distribution of social welfare payments via FinTech solutions could offer benefits in terms of transparency, particularly where the institutional capacity is low.

Advancing Finclusion in Suriname

Opportunities

Suriname has been making progress in the area of FinTech and opportunities to continue supporting adoption include: (i) The chance for government to play an important role in incentivising uptake. This can be done by offering social benefits through financial technologies. (ii) Under its E-Government strategy, the government is evaluating how electronic payments can improve tax administration to reduce informality and non-traceability. FinTech would offer benefits for this type of policy. (iii) Offering KYC clearance associated with the digital ID could help lower compliance costs for FinTech and traditional financial service providers. (iv) Suriname’s high mobile penetration rate provides opportunities to reach the unbanked with FinTech, particularly in the more remote and sparsely populated interior where it is not feasible for banks to open a physical branch.

Challenges

In our paper we also identified challenges that could hinder adoption of FinTech in the country, these include:

(i) Culture and language –The country’s cash culture challenges the adoption of digital payments. Currently, digital payments are primarily used in the capital city, whereas economic agents in remote areas tend to rely heavily on cash. Also, Suriname is multilingual, which could challenge the adoption of digital payments. People need to understand the transactions, terms of use and risks to adopt the technology.

(ii) Legislation and regulatory framework require further development to support FinTech. Currently, some FinTech solutions are being evaluated in the Central Bank’s regulatory sandbox. However, additional investment in these solutions could be limited in the absence of a legal framework that establishes the rules for companies operating in the sector. While FinTech offers a wide range of opportunities, it also could pose a risk to financial stability and integrity. To mitigate these risks, legislative reforms will be necessary.

(iii) Infrastructure – Connectivity in the interior requires investment in telecommunications and energy infrastructure as remote communities are underserved and have limited access. However, infrastructure costs could get very high due to limited road access and forest density.

(iv) Financial literacy – There are significant differences among demographic groups regarding the financial literacy rate, especially the vulnerable groups who would benefit the most from financial literacy are far behind.

Despite the challenges Suriname has been (and still is) facing, the country is promoting financial inclusion and the development and use of FinTech. There are opportunities for the IDB to contribute to this in collaboration with the government and private sector. For example, there is a need for targeted financial literacy initiatives, addressing issues that lead to lower financial literacy to help improve financial resilience. Furthermore, closing the gap between urban and rural areas with regard to access to electricity and connectivity will be important to make sure rural areas are not excluded from FinTech initiatives.

For more information on opportunities for intervention please see our paper on Financial Inclusion and FinTech in Suriname.

Leave a Reply