The global food industry loses a staggering amount annually: US$750 billion. In Latin America and the Caribbean (LAC), roughly 55 percent of post-harvest fruit and vegetables are lost, mostly due to problems arising during storage, packaging, and distribution. At the same time, high logistics costs hurt trade in food and agriculture, increasing final prices by 30 percent to 100 percent between production and delivery in LAC.

In Latin America alone, 57 percent of exports are perishable or logistics-intensive products — such as natural resources, agricultural products, and garments — compared to 17 percent in OECD countries.

Though LAC’s market share in global food exports grew from 2 percent to 14 percent between 2009 and 2016, the region has nearly 30 percent of potential arable land and the highest share of renewable water resources. In order to realize its export potential, the region will need to address food losses caused largely by its lack of appropriate cold chain logistics, infrastructure, and technical expertise.

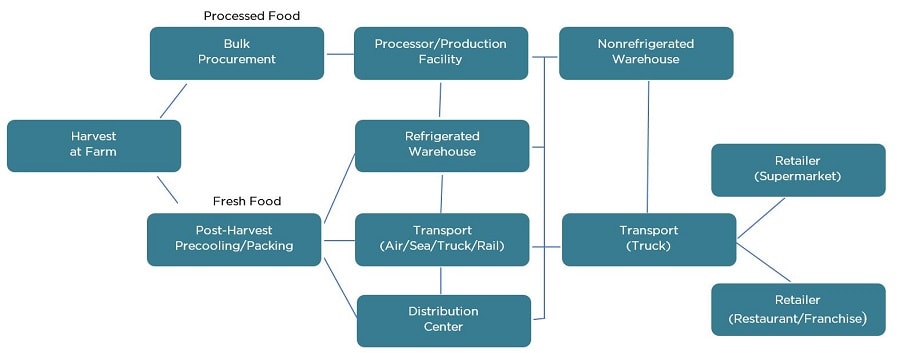

Cold chains are the use of thermal and refrigerated packing methods and logistics to guarantee the integrity of temperature and time-sensitive products transported along a supply chain. Here is an example of a cold chain flow for processed and fresh foods.

Sample Cold Chain Flow

Reproduced from 2016 ITA Cold Chain Top Markets Report.

Cold chain systems are not uniform in shape or nature; their structure depends on specific product and customer requirements. For example, different product types require different temperatures — for example, around 55°F (13°C) for fruits and vegetables but 28°F (-2°C) for meat and poultry.

Nevertheless, all cold chain structures seek to safely transport temperature and time-sensitive products to target markets while reducing waste, guaranteeing quality and integrity, and curbing contamination risk. A cold chain system can also cover the entirety or merely parts of a product’s value chain. In the case of food and agricultural goods, this refers to post-harvest activities, temperature-controlled storage, transport, and retail.

Notably, cold chain systems serve as catalysts for more exports and the opening of new markets across a wide range of sectors and over long periods of time. In this context, more cold chain capacity would benefit LAC’s pharmaceutical and medical devices industry, whose sales are expected to grow by 119 percent in between 1990 and 2021.

The quality and availability of food and agricultural products in LAC is negatively affected by inadequate cold chain capacity.

While rising export markets have been a catalyst in LAC’s improved cold chain indicators, there are great differences in the density of cold chain infrastructure across the region. Of the top 20 refrigerated warehousing and logistics providers in LAC, 19 are in the region’s food exporting powerhouses: Brazil (13), Mexico (3), Chile (2), and Argentina (1), with smaller ones scattered in Central America.

Measured as population density per cubic meter of cold chain capacity, both Chile and Panama boast numbers similar to those found in the United States and Germany — 4.2 and 7.7 versus 3.7 and 2.09, respectively. At the same time, these metrics also indicate that, overall and relatively speaking, there is still considerable room for improvement in countries such as Colombia, Venezuela, and Peru, which have densities of 497, 79, and 69, and even in better performers like Brazil and Mexico, where they stand at 35.6 and 27.9, respectively.

Human capital and knowledge are equally important, as limited or non-existent familiarity with distinct temperature needs of perishable products — primarily seen, say, in inappropriate product handling and/or exposure to wrong temperatures — can blunt the positive effects of improved cold chain infrastructure.

Cold chain structures are a function of a country’s productive capabilities and trade profile.

They are private sector investments and a function of global value chains, not an industry per se, but governments can help their development by providing appropriate hard and soft infrastructure incentives, as well as a supportive regulatory framework.

To this end, the complementarity of cold chain investments should be taken into consideration, particularly in maritime shipping, logistics, and multimodal transport. Doing so would lay important groundwork for the development of larger projects, such as cold chain distribution centers or logistics hubs near key ports in the region.

The development of cold-chain systems must happen holistically.

Doing so will ensure that newly created cold chain capacities satisfy actual demand from operators and retail markets, and are, consequently, both sustainable and profitable. In this regard, there are steps which LAC governments can take to lay the groundwork for more private investment in cold chain capacity:

- Introduce standards and policies to regulate the cold chain logistics market: the lack of end-to-end process control creates fragmented and inefficient cold chain logistics. Governments can work jointly with industry associations to create industry standards and guidelines in key sectors, such as guidelines for drug cold chain logistics or for aquaculture products (as is done in China).

- Adopt international regulations and standards: governments should adopt the International Aviation Transportation Association (IATA) Perishable Cargo Regulations to increase traceability and reduce food waste while at the same time demonstrating to export markets compliance with international standards.

- Create regulatory frameworks to support the growth of e-commerce: online grocery delivery presents a US$17 billion opportunity in LAC, increasing significantly sales of temperature-sensitive products. New models of distribution, including smaller cold storage facilities near urban centers, will grow quickly.

- Develop awareness among small agricultural actors: resources and capacity-building to small-scale agricultural producers to adopt standards and technologies would complement other initiatives targeted at boosting efficiency and streamlining access to better credit and foreign markets among the region’s vast network of family farming and agricultural cooperatives.

Leave a Reply