![]()

![]()

As the U.S. economy continues to grow and the labor market tightens, there is an increasing likelihood that the Federal Reserve will raise interest rates. The consequences will reverberate in Latin America and the Caribbean. Our research suggests there are reasons for concern, but also ways countries can offset the risks. It is key that countries in the region take this situation very seriously, as their ability to sail through turbulent waters will depend on it.

The contagion effect is well understood. Rising U.S. interest rates lower investor appetite for bonds and other securities from emerging market economies. As dollars become scarcer and more expensive, countries with large external financing needs (large current account deficits) will be more hard-pressed to obtain credit from abroad. Vulnerable countries may find themselves in the unenviable place of having to raise rates and enact painful fiscal spending cuts, even as their economies enter a recession.

Oftentimes, when one emerging economy struggles, investors tend to pull the plug on an entire class of emerging market instruments because it may not be worth their while to investigate which economies are better managed. The result is that even relatively healthy emerging economies may suffer. Because of this it is important that countries show they are making palpable efforts to improve their fundamentals.

In the past, many tightening cycles in the US interest rate have been associated with sudden, large cuts in access to credit in emerging markets, or a sudden stop, which Turkey is close to experiencing. The question is whether similar events can occur in Latin American countries. Our research on sudden stops shows there are four key fundamental variables—closely linked to liquidity—that determine if an economy is in a good position to weather the storm:

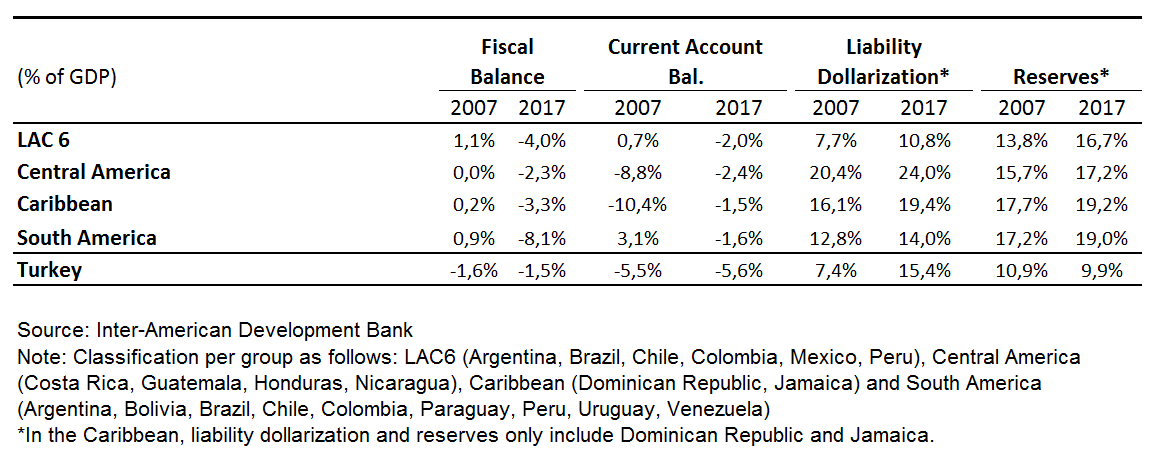

- The fiscal balance looks at the government’s need for financing. Is the government running a surplus, or is it running a deficit and heavily relies on creditors to make ends meet?

- The current account balance measures the country’s exposure to financing from the world economy. It factors in the trade balance (exports of goods and services minus imports), plus any net income and transfers from abroad. A large deficit shows exposure to credit from abroad.

- Bank liability dollarization looks at how much locals owe banks in foreign currency (usually the U.S. dollar), which may be more difficult to service if there is a large depreciation, a typical consequence of a sudden stop.

- International reserves are foreign currency assets held by the country’s central bank, which can provide liquidity at times of external shocks.

Running the numbers on these variables shows us that Latin America and the Caribbean economies are in a better position today than they were when the Tequila and Asian/Russian crises hit in the 1990s. However, they are in a weaker position compared to 2007, just before the U.S. financial crisis. On average, the fiscal balance for the six largest Latin American economies (LAC-6) was 1.1 percent of GDP in 2007. It was -4 percent in 2017. The current account balance went from 0.7 percent of GDP to -2 percent of GDP over the same period, while liability dollarization increased from 7.7% of GDP to 10.8% of GDP. On the positive side, dollar reserves rose from 13.8 percent to 16.7 percent. The table below has the numbers for different groups of countries, in comparison with Turkey, which reached a current account deficit of 5.6 percent of GDP in 2017.

The numbers suggest more vulnerability, but there are several available antidotes that countries can use:

- High international reserves. Most countries have accumulated more reserves, which act as an insurance policy against sudden stops. The optimal reserve level should strike a balance between reducing the likelihood of a sudden stop and the opportunity cost of holding reserves, just as you buy an insurance policy for your car rather than using that money on trips or vacations. Countries have built important reserve buffers, and should keep at it.

- Taking good care of local investors. Our research shows that local investors have recently played key roles in helping contain past international financial crises. During the Tequila crisis of 1994 and the Asian/Russian financial crisis of 1998, locals did not play a significant role in sudden stop episodes, which were mostly driven by foreign actors. However, in the aftermath of the Lehman debacle of 2008, locals brought substantial sums back into their local economies, helping offset capital flight by foreigners. What was different? It is all about lower confiscation risk. While this offsetting effect from locals cannot be taken for granted, local investors may respond positively, bringing their money in (and making profits), when they have assurances that their investments will not be confiscated. Sound institutions such as well-established inflation targeting regimes with low inflation levels and a consistently floating exchange rate regime, good creditor rights, and a well-functioning judiciary help bolster investor confidence. Based on a model analyzing the behavior of local investors in 48 countries during past crises, we find that for Latin America, the probability locals will offset foreign flight was about 46 percent in 2017, almost double that in 1997. It is, however, slightly less than the 53 percent mark reached in 2007.

- Most countries have floating exchange rates. The good news is that most economies have floating exchange rates, and lower liability dollarization levels than in the 1990s, which let them use their exchange rate extensively. Devaluations help boost exports and limit imports, correcting any current account imbalances. Brazil, Mexico and Argentina have survived the impacts of major devaluations this year without grave consequences so far.

- The IMF and other multilaterals can provide resources to help tide a crisis. Mexico has a large flexible credit line (FCL) that it can draw on in case of a sudden stop. Argentina has just negotiated a package with the IMF. Such packages can carry political costs, but we believe countries come out ahead. The sum of high international reserves plus multilateral support is a powerful signal to investors that the country is in a better position to avoid a sudden stop.

- While the fiscal front has deteriorated in recent years, there are opportunities to spend better, making fiscal consolidation less costly on output. This time most governments will have little budget room for counter-cyclical policies. When deciding on fiscal consolidation, they should avoid cutting back on capital expenditure, such as infrastructure, because this type of expenditure has the largest fiscal multiplier. Although consolidation requires a lot of effort, the good news here is that there are large potential efficiency gains from using resources better rather than resorting to painful, across-the-board cuts. Our upcoming publication on how governments can spend smarter will address this very issue. In potential times of distress, Governments will also find it useful to signal their commitment to fiscal prudency by announcing policies that will be implemented in the future, even if they cannot be implemented right away.

While the global economic context is a challenging one, we believe countries have some of the required tools to avoid the dreaded sudden stops. Yet they need to keep working at it—particularly on the fiscal side—so that they can place themselves in the best possible position to withstand a potential worsening in external financing conditions.

Leave a Reply