Global financial markets are at a crossroads, subject to increased short-term uncertainty as well as structural shifts, both of which pose risks to the macroeconomic and development outlook of emerging economies.

To start with, central banks around the world are aggressively tightening monetary policy to fight inflation. This has complex ramifications for exchange rate markets, credit risk (both sovereigns and companies) and pricing across asset classes and financial instruments. It may affect capital requirements for financial institutions, investor risk appetite, and other dimensions of the global financial system.

Longstanding geopolitical rifts have also been amplified by the war in Ukraine, which has triggered discussion about numerous aspects of the international financial system. These include the future status of global reserve currencies, the evolution of cross-border payment systems, financial/investment arrangements for strategic sectors such as food and energy, and the reshaping of capital flow patterns.

Against this background, a revamped global financial landscape that impacts both the cost and availability of financing for sovereigns and companies is in the making. A profound uncertainty reigns as to how such a landscape will evolve. But governments will be called to react and adapt, and, in the process, they will need solid macroeconomic buffers to cope with the shocks.

Quantifying the Impact of Global Stress in the Southern Cone

Global financial shocks in this new landscape can have unexpected, multi-faceted, and disruptive implications for emerging market economies. In a new study for the Southern Cone countries, we use a simple and direct approach to quantify the potential impact of global financial stress on sovereign spreads for Brazil, Chile, Paraguay, and Uruguay, and compare them with other countries.

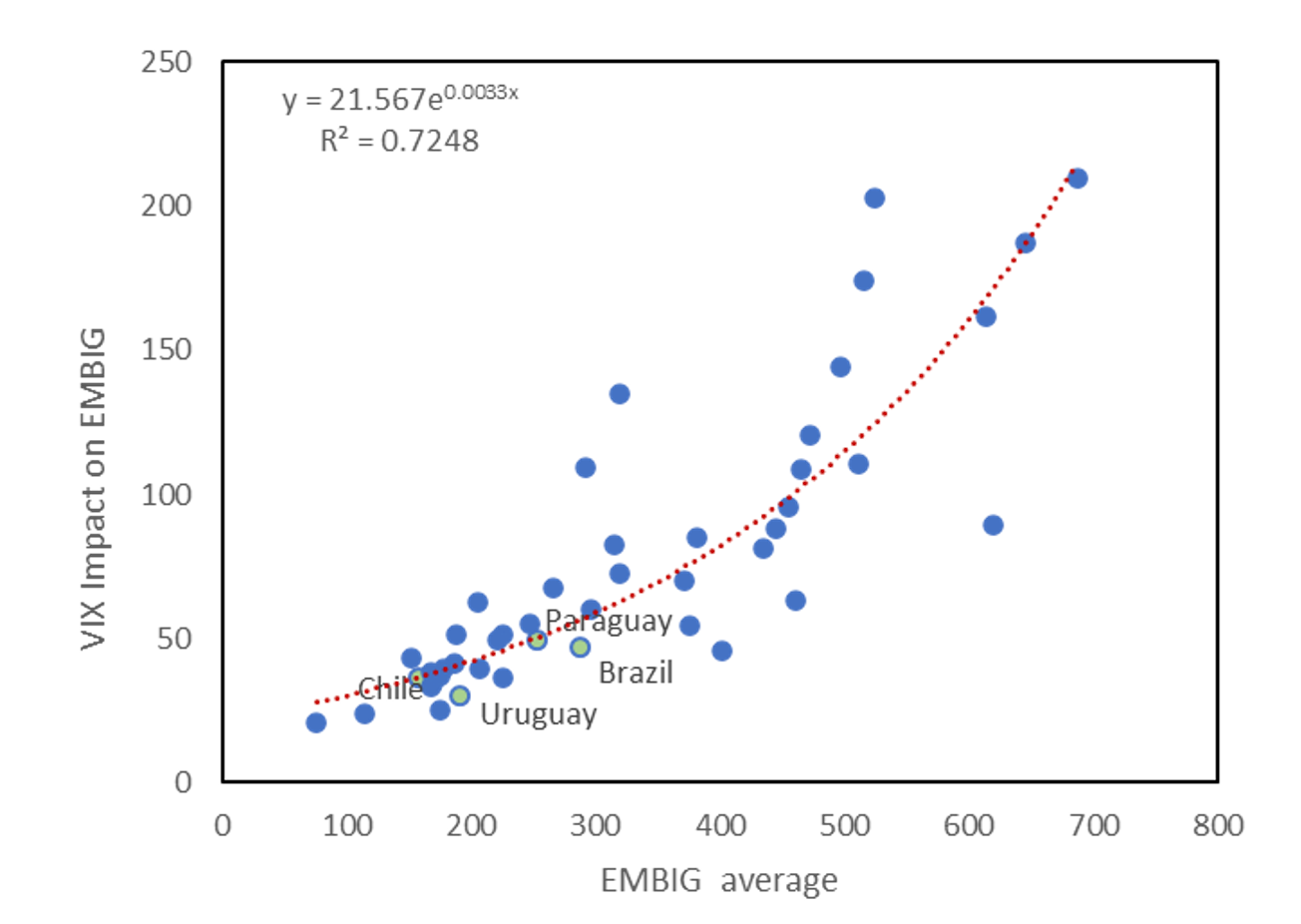

Using the VIX volatility index[1] as a proxy for global financial stress, we argue that macro conditions in the Southern Cone can experience significant pressure amid adverse global financial shocks. A “normal-sized shock” to the VIX (approximately 7 VIX points) increases the region’s sovereign spreads between 30 and 49 basis points over a 3-month horizon as depicted in colored circles in figure 1. These effects could be more than 6 times stronger with acute shocks such as the ones that occurred during the 2008-09 Global Financial Crisis or at the beginning of the pandemic.

Moreover, smaller financial shocks could also generate significant macro stress if exacerbated by other domestic vulnerabilities. Macro stress in the region could be further amplified if global financial shocks were combined with a global recession/slowdown that negatively affected commodity prices.

Figure 1: Accumulated 3-Month Impact on Sovereign Spreads

Basis points

Many factors are not incorporated in our exercise, including policy responses that can have a mitigating role during a crisis. But uncertainty about the estimates cuts both ways. Our econometric exercise does not feature explicit transmission channels responsible for feedback and indirect effects. Those channels could be more worrisome today than in the past, and not controlling for them leads to an underestimation of the total impact. In fact, global financial shocks could interact with domestic economic, social, and political vulnerabilities that have been growing in the region -and in other emerging economies- amplifying the consequences of global uncertainty.

The increase in global interest rates acts as another source of financial shock, increasing borrowing costs in emerging economies. And with today’s strong inflationary pressures, it could be harder for monetary authorities in the region to reverse course and resort again to extraordinary monetary expansion to stabilize financial market disruptions. For Southern Cone economies, all else being equal, this would translate into weaker capital inflows and less favorable financing conditions.

Finally, the figure shows that countries that have a higher risk level to start with (higher levels of EMBIG spreads as depicted along the X-axis of figure 1) experience a stronger impact in terms of country risk when hit by a global financial shock. Such relationship between sensitivity and level is particularly relevant for the four Southern Cone countries since they are still at a range of the EMBIG in which this non-linear relationship is not kicking in strongly. However, should Southern Cone countries be hit by a sequence of negative global financial shocks that increases the country risk base level, sovereign spreads could increasingly deteriorate triggering significant macro stress.

Rebuilding Macro Buffers to Weather Financial Risks

Southern Cone countries would benefit from rebuilding macro buffers now to weather the risky global financial environment ahead. Rebuilding macro buffers should be seen as being equally important to other public policies, and short-term trade-offs among them should be transparently communicated and discussed.

What exactly are policy-relevant macro buffers? In general, to stave off perceptions of risk, countries could benefit from more transparent fiscal frameworks assuring fiscal consolidation, active debt management and enough liquidity buffers (where reserves and contingent loans are good alternatives). But plans to rebuild macro buffers should be tailored to each country and, most importantly, be considered as an integral part of broader strategies to support medium-term, sustained inclusive growth as well as the materialization of the region’s productive potential in a context of greater inequality, poverty, and social demands.

International organizations, including multilateral development banks, can play a crucial role helping to rebuild macro buffers. They can help to strengthen contingent credit lines and, along with other institutions, help to mitigate fiscal risks by encouraging greater public sector efficiency and hedging against commodity prices or climate shocks. Moreover, they can mobilize private sector investment and encourage greater cooperation among the region’s countries, which would also help to achieve greater resilience against financial shocks.

[1] The Cboe Volatility Index, or VIX, is a market index representing the market’s expectations for volatility over the coming 30 days. Investors use the VIX to measure the level of risk, fear, or stress in the market.

Leave a Reply