Despite recent improvements, the Caribbean region is still grappling with headwinds affecting social dynamics, fiscal outcomes, and economic growth. Global commodity prices—particularly for food and energy—remain volatile and above pre-pandemic levels, straining household budgets. While true that tourism dependent economies have seen this crucial sector recover, and commodity exporting governments have benefited from elevated prices, many citizens—particularly the most vulnerable— remain under strain.

Against this backdrop, policy makers across the region have begun to consider policies aimed at increasing competitiveness and developing closer economic relationships with regional partners, including near-shoring (particularly, global services), and deeper regional integration (with an emphasis on agriculture). The latest edition of the IDB’s Caribbean Economics Quarterly (August 2023) highlights these and related challenges and opportunities for the region.

In this blogpost, we highlight the key findings of this economic report:

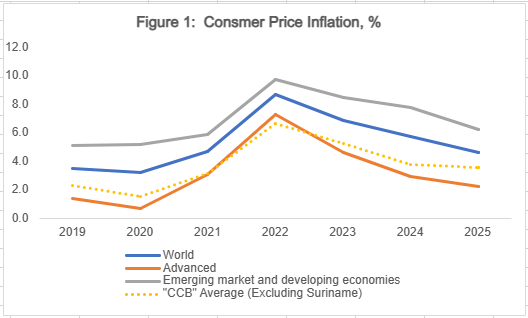

- Inflation has subsided, but remains above than pre-pandemic norms

Inflation remains a challenge globally. Even advanced economies have struggled to tame inflation, despite aggressive responses from central banks. Although inflation in 2023 is projected to be significantly lower than in 2022 across advanced, emerging, and developing economies, it is expected to remain noticeably above pre-pandemic levels up until at least 2025. The Caribbean is particularly vulnerable, given that most countries are net importers of fuel and food.

- Despite high inflation, the recovery in the Caribbean was robust in 2022

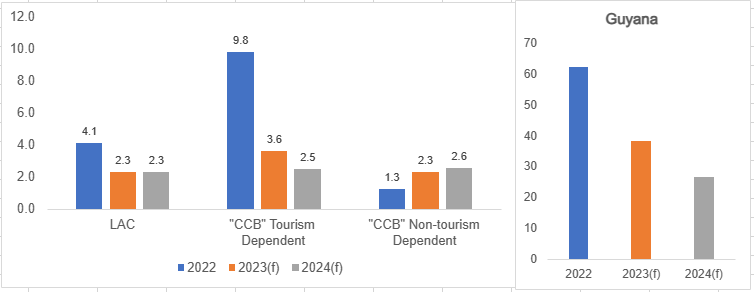

Regardless of these persistent challenges and nascent opportunities, the Caribbean—both tourism- and commodity-dependent economies—, has broadly recuperated most of the lost economic activity since the pandemic (Figure 2). Commodity exporters have weathered the pandemic with fewer dislocations than their tourism-dependent neighbors. Guyana in particular will continue to benefit from an oil-driven boom for the foreseeable future.

Among tourism-dependent Caribbean states, tourism arrivals in Jamaica and The Bahamas have already surpassed their respective pre-pandemic levels. Nevertheless, it is unclear if the strength of tourist arrivals will be transitory—that is, a “binge effect” driven by pent-up demand from the pandemic—or permanent—that is, structural changes such as remote work increasing the number of visitors blending leisure and labor. Consequently, the onus will be on regional policymakers to implement the necessary reforms to capture the upside of these structural changes in source markets.

- High inflation remains a significant risk over the short- to medium-term

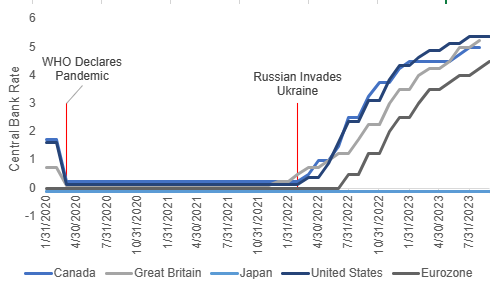

Despite a better-than-expected recovery in the region, several macroeconomic risks remain evident and increasingly acute. High inflation has caught the attention of central banks, particularly those with inflation-targeting mandates. In a span of less than 18 months, policy rates have risen by almost 500 basis points (Figure 2). Despite the recent pause led by the Federal Reserve, central banks, except for Japan’s, are expected to continue their policy rate hikes as a response to persistent inflationary pressures. Additionally, increased policy rates could increase the borrowing costs for multilaterals, which is an important source of financing for several Caribbean governments. In the short- and medium-term, increased rates could also reduce the spending appetite by households in source markets for tourism, and could lead to a slowdown in arrivals as households prioritize saving. This reduction in spending could affect tourism-dependent economies in the Caribbean, and thus negatively affect growth. Furthermore, reduced spending by both households and businesses could reduce demand for commodities, such as oil, which would also negatively impact commodity-exporters, including those in the Caribbean.

- The Caribbean is highly vulnerable to climate change

Another particular risk includes climate change, which Climate change disproportionally affects the Caribbean through several channels. One of the more relevant channels is the annual hurricane season, which is still active for 2023. The National Oceanic and Atmospheric Administration (NOAA) has recently updated its forecast, and is now expecting an “above normal” season, and the season is still with us. A single, devastating hurricane can derail the recovery for one or several island states. Another channel is the El Niño phenomenon, which can cause unusually dry and hot conditions, and further encourage the formation of hurricanes. Both these channels can be particularly destructive to the agriculture sector within the Caribbean, which is currently confronting a food security challenge.

- Food security is a rising concern for the Caribbean

Other risks for the region include geopolitically driven economic impacts (including “slowbalization”), and further global commodity price shocks, particularly for food. In the case of the former, supply-chain disruptions in the short-term could lead to offshoring opportunities for the Caribbean, such as Jamaica, which is geographically close to major markets such as the United States. In the case of the latter, food security has become a priority for several Caribbean islands and there is currently a concerted push to stimulate the agriculture sector at the regional level as demonstrated by the recent CARICOM summit. Nevertheless, whether these current risks become future opportunities will depend largely on the proactive efforts of regional policymakers.

Leave a Reply