According to Trade Trend Estimates: Latin America and the Caribbean, in 2016, exports from Latin America and the Caribbean have shrunk by an estimated 6%, which points to a tempering of the severe 15% contraction of 2015. Almost every country in the region saw a slowing in the pace of the contraction of foreign sales (Figure 1). Remarkably, starting from August 2016, the region started to witness some positive year-on-year growth rates for the first time in 22 months.

The Value of Latin American and Caribbean – Exports and World Trade (Quarterly moving average of the year-on-year growth rate, percentage, 2014–2016)

Source: IDB Integration and Trade Sector based on data from official sources and the Netherlands Bureau for Economic Policy Analysis (CPB) for world trade.

Note: LAC includes 18 countries in Latin America — Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, El Salvador, Guatemala, Honduras, Mexico, Nicaragua, Panama, Paraguay, Peru, Uruguay, and Venezuela — and six countries in the Caribbean — Barbados, Belize, Guyana, Jamaica, Suriname, and Trinidad and Tobago. World trade is the average of global imports and exports.

After four consecutive years of uninterrupted contraction in global trade, what factors are behind this relative improvement in export performance? Can we expect exports to start growing again in the near future? Is this reversal in trends sustainable? What risks is the region facing into the future?

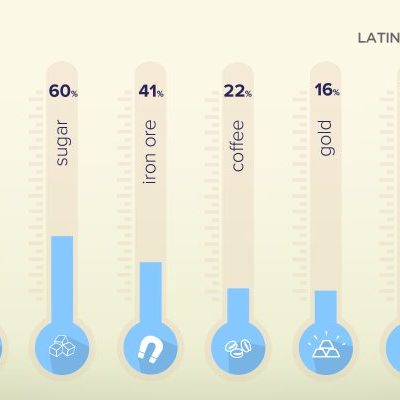

The slowdown in the rate of export decline is mainly due to the stabilization of commodity prices, which seem to have bottomed out and are even showing signs of recovery in some cases, such as petroleum, coffee, and oil.

Although the recent OPEC agreement should boost the price of crude oil over the coming six-month periods, the evolution of other commodity prices remains uncertain. An upturn in the global economy supported by the economic expansion of the United States may help shore up this process, but the foreseeable appreciation of the dollar will continue to affect the prices of the region’s main export products.

However, the growth in the region’s export volumes fell short of causing a significant improvement in trade performance. The information available for nine countries shows a slowdown in the growth of export volumes for the first three quarters of 2016. The cumulative year-on-year variation was 2.1% for this group, compared to 4.2% in 2015. The exceptions to the rule were Brazil and Peru, which took advantage of unique circumstances to increase exports of sugar and copper, respectively; and Argentina, which saw a leap in real exports at the start of the year following the devaluation of the peso, although this turned out to be short lived.

Monthly Export Volumes for Selected Countries (Index, 12-month moving average, January 2014=100, 2014–2016)

Source: IDB Integration and Trade Sector based on data from official sources and the US Bureau of Labor Statistics (BLS) and the Organization of Petroleum Exporting Countries (OPEC).

Note: The value of Mexico’s exports was deflated using BLS indices, and the volume of Venezuela’s exports was estimated using OPEC data. LA-9 is the average of national indices weighted by the value of each country’s exports in 2015; the sample represents 91% of LA’s foreign sales for that year.

The combined impact of the evolution of prices and export volumes points to a mixed outlook for the region. There was a marked deceleration in the downturn in exports in South America, where the estimated contraction of 8% in 2016 is far below the 23% drop of 2015. In Mesoamerica, foreign sales are expected to shrink by 3%, a rate similar to that of 2015. The rate of export decline has yet to slow in the Caribbean, which saw an estimated drop of 21% in 2016, similar to the 22% fall of 2015.

On the demand side, 2016 brought significant variations in demand from the region’s major trade partners in comparison with 2015.

The contraction in exports was particularly affected by lower demand from within the region and from the United States, but less so by demand from China, the rest of Asia, and the European Union. The slump in intraregional demand had a marked effect on the economies of South America and looks set to continue, while the economic growth in the United States was not channeled through trade, which had a negative effect on the performance of Mexico and Central America.

Looking to the future, the risks ahead for the region’s export growth are smaller but still tilted to the downside.

The possibility of a reversal in the current downward trend depends on whether commodity prices continue to improve despite the foreseeable appreciation of the dollar, and on whether the region returns to a path of growth thereby reigniting intraregional trade. An acceleration in external demand, particularly from the United States and China, would bolster exports, while a return to protectionism would skew this forecast in the opposite direction.

In short, Latin America and the Caribbean seem to have moved past the worst stage in the trade slump now that the global outlook appears to be improving. However, as is analyzed in detail in the Trade and Integration Monitor 2016, whether or not this recovery is sustainable will depend fundamentally on the capacity of the region’s economies to overcome the structural shortcomings that characterize their trade specialization and their excessive dependence on commodity exports.

These challenges are even greater in an economic context marked by a decrease in the region’s capacity to grow by leveraging the growth of the rest of the world via trade, and in a political context that is increasingly skeptical of the benefits of openness, particularly in advanced economies.

Leave a Reply