![]()

On November 2, 2017, the Bank of England increased its policy interest rate from 0.25% to 0.5%. At the same time, it issued the sternest warning yet that Brexit would have a negative impact on the economy. The statement made the markets think that the economy was weaker than previously thought, or that the Bank of England might be more dovish than expected in the future. The rate rise was largely expected and the pound depreciated (Giles 2017, Rees 2017). [i]

On June 22, 2017, the Banco de Mexico raised its policy rate by 0.25%. This was despite negative economic news, especially regarding the renegotiation of the North American Free Trade Agreement that may have significant macroeconomic impact. This was the seventh rate-rise in Mexico in as many monetary policy meetings, bringing the policy rate to 7%. The statement hinting this might be the end of the tightening cycle was perhaps the news event, rather than the rise itself.

Is inflation targeting really supposed to work like this? Are policy rates really supposed to be raised when there is negative news regarding the economy? Don’t most models suggest the opposite? The recent experience of several Latin American inflation-targeting regimes has been fascinating and may have lessons for the UK and other countries. This blog considers Latin American cases and suggests the theory underlying inflation targeting may need to be reconsidered.

Latin American Inflation Targeting in Practice

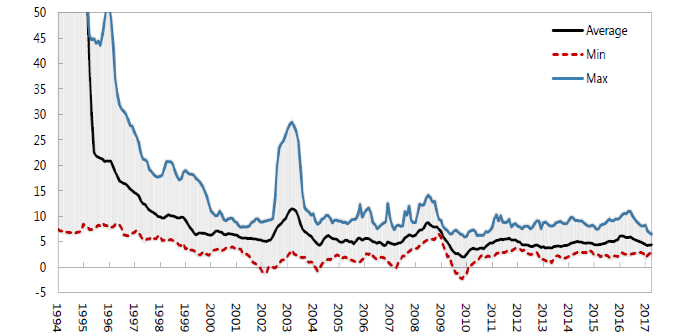

Figure 1 plots minimum, maximum and average inflation levels across eight Latin American inflation-targeting economies: Brazil, Chile, Colombia, Guatemala, Mexico, Paraguay, Peru, and Uruguay. It illustrates how inflation came down and has remained largely under control. [ii] While there are variations across countries, Mariscal et al. show that on average these eight regimes gained considerable credibility, and that the impact of current inflation shocks on medium-term inflation expectations fell.

Figure 1. Inflation Rates in Latin America (% per annum)

Source: Mariscal, Powell and Tavella (forthcoming)

Figure 2 plots the coefficient on current inflation in a rolling regression for medium-term inflation expectations. While at the start of the sample the coefficient is significant, it then declines until statistical tests cannot reject that it is zero.

Figure 2. Coefficient on Current Inflation in Latin America

Source: Mariscal et al (forthcoming). Figure plots the coefficient on current inflation and error bounds for that estimate in a rolling panel regression for medium term inflation expectations.

In the period after the Global Crisis, however, there were further negative shocks. For the economies of Chile and Peru, copper prices, which are particularly important, fell sharply from 2010. For Colombia, the collapse of oil prices two years later was key. For Mexico, a mix of oil prices and concerns over future US trade policy affected fiscal accounts and prospects for investment. Brazil suffered a major political crisis and weaker prices for iron ore and grains. Paraguay and Uruguay’s shocks came from their larger neighbors (Argentina and Brazil) as well as weaker agricultural prices.

These shocks provoked large nominal currency depreciations in some countries. While pass-through was moderate, it was not zero and inflation rose. In several cases, inflation breached the relevant inflation target.

How did central banks respond? In several cases they increased policy interest rates—a move that is sometimes labelled procyclical monetary policy (Vegh and Vuletin 2016). But while interest-rate policy was procyclical in some cases, it responded to large depreciations which likely favored domestic production. In fact, as in the UK, the initial impact on exports appeared to be negative. This is especially true if exports are valued in dollars, but it was also true for volumes. Only recently have the depreciations started to produce positive effects, but a notable fall in import penetration has aided domestic production [iii] . Thus, the monetary stance, taking into account exchange rate movements, was possibly even countercyclical in nature [iv].

Should Central Banks Have Acted in this Way?

One argument is that such a depreciation should be considered a temporary shock, and inflation would naturally dampen anyway. But a fundamental indeterminacy exists in monetary models. Only the ratio of money and prices is pinned down, so this argument does not necessarily hold. But if there is an explicit target, and inflation is pushed above that level, then it might be argued that it will come back down, especially if everyone trusts the central bank to publish forecasts to that effect. Or, to put that in a more sophisticated way, inflation should come down if the central bank, through its communication strategy, maintains a focal point for expectations around its target.

But if inflation persists above a target, and a central bank doesn’t react, the credibility of the regime might be tested. Why would expectations remain anchored at the target if central banks don’t actually react? This highlights the difficult nature of expectations’ equilibria. Moreover, we found that when inflation is above the relevant target, inflation shocks had greater impacts on medium-term inflation expectations.

Taking a step back, most inflation-targeting regimes in Latin America emerged from systems of fixed-exchange-rates or exchange-rate bands. The first to target inflation was Chile from the early 1990s. Central banks in Latin America adopted inflation targeting to establish a nominal anchor that was not the exchange rate, so countries could enjoy both an anchor and exchange rate flexibility. As the recent experience highlights, exchange rates have in general been very flexible and this has been valuable. Compare, for example, the response of Ecuador and Colombia to recent oil price shocks. Ecuador uses the US dollar as its currency, and suffered a major recession. Colombia could make use of its flexible exchange rate to dampen the impacts (see IDB, (2016).

But exchange-rate flexibility can only be maintained if the anchor is credible. If not, pass-through may rise, and inflation would render nominal depreciations ineffective. Our paper suggests that there is a cost to allowing inflation to rise above a target [v]. Figure 2 shows that the coefficient on current inflation shocks was already creeping towards positive and significant territory toward the end of the sample, indicating a risk that expectations might become de-anchored.

In IDB (2017) we developed ideas from Christiano et al. (2005) and Fernandez et al. (2015) to create a fully-fledged neo-Keynesian monetary model, calibrated on five of the larger inflation-targeting regimes in Latin America, assuming full credibility. In simulations, we tested a less-restrictive monetary policy in the face of negative shocks relative to actual (estimated Taylor-type) rules.

The results were surprising. As the private sector knows and anticipates the new, less-restrictive rule, demand is higher than it would otherwise have been, and so is inflation. It is as if the pass-through had become stronger. As inflation rises, the central bank has to react anyway, because it still cares about inflation and the model assumes a fully credible target. The result is a higher inflation path, but very little gain in output. While we will never know the counterfactual for sure, perhaps on balance central banks were right to be cautious and raise interest rates, despite the negative economic news.

The bottom line: the output gain of a less restrictive policy may have been low, but inflation may have been higher for longer. That might have posed a danger to the credibility of the target, which might then have restricted exchange rate flexibility and the possibility of a countercyclical monetary stance in the future.

What Does This Mean for the UK, and for Economic Theory?

The unexpected Brexit vote, and the uncertainty as to what the final Brexit deal will look like, provoked a depreciation of the pound which has raised inflation. To date, the depreciation of the pound has not had a strong positive impact on exports, and the trade deficit soared.

The Latin American experience was similar, but over time the fall in import penetration became a key mechanism for depreciations to help output. The beneficial impact on exports happened much later. While the Brexit shock is different, the recent decision of the Monetary Policy Committee is not a huge surprise given the Latin American experience. The procyclical interest rate rise must be placed in the context of a much weaker pound, and not considered in isolation.

Some elegant models see inflation targeting as a flexible, and under some conditions, even an optimal policy rule (Giannoni and Woodford 2004, and other chapters in Bernanke and Woodford 2004). But models that do not capture the role of expectations and a potential loss of credibility tell only part of the story. Recent experience also highlights that for small open economies the role of the exchange rate, frequently pinned down by equations that rarely hold in practice, is key. In short, work remains to be done for the models to catch up to the fascinating experience of inflation targeting in recent years.

Note: This blog was first published in English in VoxEU

Endnotes

[i] The rate rise discussion had been going on for some months. The conclusion of the Monetary Policy Committee meeting ending 14 June 2017 was to not to raise rates, but it was a close call: the vote was 5 to 3.

[ii] Inflation in Mexico has been over target, but it has been falling in most of Latin America. On 29 June, Brazil announced a reduction for its inflation target for 2019 from 4.5% to 4.25%. Current inflation was 3.6% compared to 11% at the start of 2016.

[iii] Import penetration fell across countries at an economy-wide level, considering manufactured good sectors across countries and also considering sub-sectors within manufacturing indicating that the result was not just due to changes in composition – see IADB2017), Appendix D. The impact on exports was less pronounced, but considering the exchange rate movements of competitor countries that export similar products to the same export destinations, ‘competition-adjusted’ real exchange rates depreciated less than other measures (Stein et al. 2017 and IADB 2016).

[iv] To make this precise: procyclicality in interest rates seems to be defined as whether they rise or fall. A minimal argument is that if the rate rise is a response to pass-through from a depreciation, then the impact of the depreciation on output should be taken into account.

[v] We introduced a regressor of whether current inflation was above target-plus-1% in the rolling regression to explain medium-term inflation expectations. This term was positive and significant in the middle of the sample.

Leave a Reply