In 2008, Jamaica was hit by the world economic downturn when it was already plagued by years of weak economic performance as well as high and increasing debt levels. As a result of the additional pressure from the global financial crisis, Jamaica’s fiscal situation quickly became unsustainable. Starting in 2010, Jamaica’s government took decisive actions, including two domestic debt exchanges, to bring its debt trajectory on a more sustainable path.

Today, Jamaica’s economy has stabilized, debt-to-GDP has been steadily declining, and the country is projected to grow at an average of 2.1 percent over the next years. Given Jamaica’s highly successful fiscal consolidation and performance over the last 6 years it is easy to forget how vulnerable the situation had been in 2012 and early 2013. With the unsustainable level of debt that Jamaica had been facing during the global financial crisis, the two debt exchange operations – the 2010 Jamaica Debt Exchange (JDX) and the 2013 National Debt Exchange (NDX) – were central to Jamaica’s successful stabilization and its path towards steady economic growth.

To share these lessons, I recently updated and translated into Spanish a 2016 policy brief that compares and discusses these two domestic debt exchanges. Jamaica’s experience offers important lessons for countries with high and/or increasing debt levels, especially when these include significant amounts of domestic debt. Below are four key lessons learned:

- Domestic debt can create a dangerous link between the health of government finances and the stability of the financial sector: A major issue in the case of Jamaica was the high exposure of the financial sector to government debt, creating a link between the fiscal situation and financial sector stability. In addition, the unique composition of Jamaica’s debt restricted debt operations to domestic government securities, which comprised around half of total debt. Any attempt to restructure the nation’s debt stock through a deep intervention, such as a reduction in the face value of the debt, would likely have had a substantial impact on the domestic financial sector.

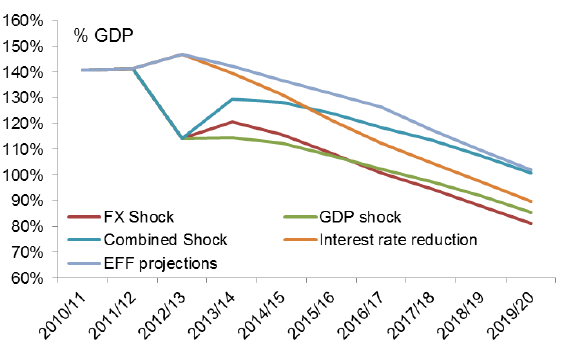

- Even aggressive debt interventions can result in only small fiscal gains: Losses within the financial sector would likely have negative multiplier effects on GDP growth, employment, and poverty – making a stabilization based on a debt operation alone an elusive goal. The graph below highlights that point in that it simulates Jamaica’s debt-to-GDP trajectory after a 50% value reduction of domestic debt under different macroeconomic scenarios. While the face value reduction would have led to an immediate, large drop in the debt-to-GDP ratio, the likely economic consequences in terms of GDP contraction and exchange rate movement would have undone an important part of the effect. As a result, the fiscal adjustment that had been foreseen under Jamaica’s four-year Extended Fund Facility with the International Monetary Fund, and the more aggressive option would have resulted in similar levels of debt-to-GDP as of March 2020 (see how the blue and the purple line reach the same level as of 2019/20).

Debt Trajectory after 50 Percent Face Value Reduction and Shocks Source: Figure 5b in Schmid (2016) - The support of the financial sector is crucial for long-term sustainability following domestic debt exchanges. While both exchanges were voluntary, there was an important difference in perception between the 2010 JDX and the 2013 NDX operations. The JDX had not only been seen as a one-time event; there was also the perception that interest rates on these securities had been excessively high in the period before the exchange. As such, the JDX was seen as necessary, even by the holders of the securities, and the government was able to access domestic financing shortly after the exchange. However, the same was not true for the 2013 NDX. February 2013 would have been the first time in three years that investors would have been paid out following the 2010 debt exchange, but the NDX extended the maturity of most of the domestic securities. In addition, yields were already lower than at the time of the JDX. Conversely to the period following the JDX, interest rates quickly started to increase while the domestic debt market became inactive without any government issuances and virtually no secondary-market trading for an extended period, which brought about challenges for the Jamaican Government.

- Decisive action can avoid long-term vicious circles. With hindsight, the 2010 JDX should have led to a stronger reduction in the debt burden. Not only did interest rates decrease after the JDX, but the interest payments still posed a high burden on the country and a second debt exchange was required only three years later. Jamaica would probably have been better off if it had done the JDX more aggressively without the need of the NDX three years later.

Taking these lessons together: The scope of fiscal savings from debt restructuring in the absence of financial sector crisis can be small in countries that rely on domestic financing. However, if unsustainable situations build up, as had been the case in Jamaica with its high debt and an excessively high interest burden, holders of debt can be supportive of decisive actions, even if it involves short-term losses. While it is difficult to find the right balance between fiscal savings and short-term pain, decisive actions can be very beneficial and will avoid repeated and failed attempts by governments to avert fiscal crisis.

Read the policy brief in Spanish or access the original 2016 policy brief in English.

Leave a Reply