Caribbean countries face serious fiscal and debt challenges. As recorded in the most recent OECD Latin American and Caribbean Economic Outlook 2018, two Caribbean countries hold the highest debt in the region: Barbados and Jamaica.

Public debt by currency and legislation, circa 2016 (central government, % of GDP)

Source: OECD Latin American and Caribbean Economic Outlook 2018

These trends are not new. During the 1990s, an analysis by the World Bank noted that: “In almost every Caribbean country, public sector debt is an issue, with public sector debt levels rising sharply since 1997 from already high levels” (2005: 33). A 2017 study from the Inter-American Development Bank (IDB) noted that debt trajectories have worsened since the 2008 crisis. General government gross debt in Caribbean countries grew to an average 73% of GDP in 2009 (almost seven percentage points higher than the average debt to GDP ratios in 2007) and have since continued to rise, reaching 76.7% of GDP in 2016. Despite each country’s unique circumstances, procyclical fiscal policy, institutional weaknesses, inadequate planning and recurrent fiscal mismanagement, have been highlighted as the most important causes behind these trends.

What can Caribbean countries do to mitigate fiscal imbalances and rising debt?

Fiscal rules are a popular measure that countries turn to in recent years., Fiscal rules have been at the center of fiscal management discussions for some time, and their application has surged in recent years. Fiscal rules are defined by the International Monetary Fund (IMF) as “a long-lasting constraint on fiscal policy through numerical limits on budgetary aggregates.”

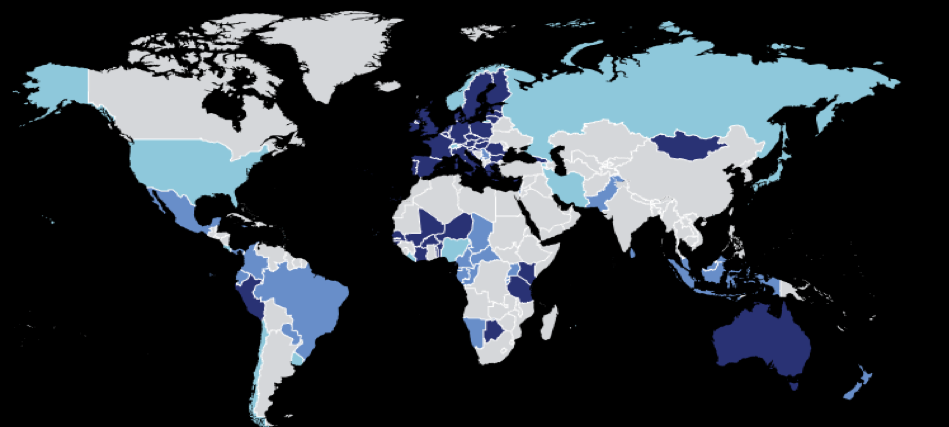

The number of countries using one or more fiscal rules increased from 5 to 76 between 1990 and 2012. Many developing countries have jumped on this bandwagon in the hopes of finding a solution to unsustainable fiscal policies. Currently, only two countries in the Caribbean have national fiscal rules in place (Jamaica and Grenada. They are thus an under-utilized tool which could potentially ease the Caribbean region’s fiscal and debt woes. But are fiscal rules really the solution?

Map of Countries with Fiscal rules: in 1990 vs in 2015 from Caribbean Country Department IDB.

Note: The color shade denotes the number of fiscal rules in place. Darker tones of blue represent more fiscal rules.

Source: IMF Data mapper – Animated by Lynn Saghir

A large body of research has found evidence that, in the presence of political commitment and strong institutional structures, well-designed fiscal rules can indeedpromote fiscal discipline through several channels:

- Acting as a commitment device, by limiting government’s use of fiscal discretion.

- Enhancing the credibility of governments by signaling their commitment to fiscal prudence.

- Playing the role of a signaling device, by enhancing transparency and revealing the preferences and fiscal plans of the government to the public and financial markets in a context of imperfect information.

- Serving as a contract to facilitate the formation and stability of political coalitions, in some cases.

However, poorly designed fiscal rules can be more harmful than helpful.For example, budget and deficit rules could force cuts in investment, accommodate currency manipulations, and not guarantee debt sustainability; whereas debt rules may lead to undesirable responses to interest rate and exchange rate shocks, if debt is close to its prudential limit.

Breaching fiscal rules is also common, particularly during economic downturns. This can have further negative effects on investor confidence and sovereign spreads. A recent IMF working paper found evidence that breaching the fiscal rules in European countries has been more the norm than the exception in recent years. Noncompliance rates rose from 21% in the pre-2008 crisis period to 63% in the post-crisis period. Although introducing sanctions for non-compliance in the design of fiscal rules is generally recommended, the reality is that imposing sanctions for breaching fiscal rules during economic downturns is likely to further burden countries which are already struggling.

Caribbean countries would therefore be well-advised to take the experience of European countries into account, when thinking of implementing fiscal rules themselves. Fiscal rules should be: (i) simple; (ii) credible; and (iii) enforceable. Most importantly, there must be political buy-in, both from politicians and from citizens, as well as strong institutional foundations to ensure their full adoption and enforcement. Communication and inclusion are thus key. Otherwise, the remedy could be worse than the problem.

There are no magic solutions to the Caribbean’s fiscal woes. The key will be for countries to set clear fiscal prudence strategies and have the discipline to adhere to them, irrespective of political or economic cycles. Fiscal rules are definitely a good tool towards this end, but they require a sound technical approach, public buy-in, and political commitment.

Note: Currency Union have also set supranational fiscal rules since 1998. Further information is available here.

About the author

L aura Giles Álvarez is a young professional at the Inter-American Development Bank. She previously worked in the Social Protection and Health Division and is currently working with the Country Economist Team for Barbados. She has worked as a development economist in Asia, Africa, and Latin America, focusing on public financial management and fiscal policy.

aura Giles Álvarez is a young professional at the Inter-American Development Bank. She previously worked in the Social Protection and Health Division and is currently working with the Country Economist Team for Barbados. She has worked as a development economist in Asia, Africa, and Latin America, focusing on public financial management and fiscal policy.

Leave a Reply