The COVID crisis has generated an unprecedented fiscal response as the total resources assigned to attend the pandemic globally has reached $11 trillion, according to the World Economic Forum. Latin America and the Caribbean (LAC) has not been an exception. Taken together, the announced measures in LAC amount, on average[1], to 8 percent of the region’s GDP as stated by the IMF.

While such spending was needed to address the social, health and economic impacts of the crisis, this vast expenditure has caused a profound deterioration of fiscal balances. Implementation of the support packages is expected to lead to large fiscal deficits which has resulted in large financing needs in 2020 that have been partially covered by countries taking on additional debt.

Among the five major countries, gross financing needs range from about 10 percent of GDP in Chile, Colombia, and Peru, to over 25 percent of GDP in Brazil, according to the IMF. Part of the response measures has been the suspension of fiscal rules in at least 60 percent of the countries that had such rules active in the region.

Such large budget deficits and rising debt levels could become a drag on sustained economic recovery if governments do not take measures to reign on them and send investors a clear signal that they will manage public finances responsibly. A good place to start is restoring the fiscal rules. In this blog, we will explain why fiscal rules are needed and we will show how this measure can support the post-pandemic recovery.

The Importance of Fiscal Rules to Build Credibility

The economic literature has been forceful on the role of fiscal institutions in attenuating economic fluctuations. In particular, the implementation of fiscal rules has gained importance in the toolkit of macroeconomic stabilization policies.

While different arrangements coexist, the main objective of fiscal rule implementations is the same: they seek to confer credibility on the conduct of fiscal (and, more in general, macroeconomic) policies by removing discretionary intervention[2]. The central idea is that such rules will allow a country’s macroeconomic fundamentals to remain solid and stable regardless of the government in charge.

While the fiscal discipline has long been highly regarded, governments may have incentives to overspend under certain circumstances, creating large public budget misalignments. For instance, governments can see active public spending as a way of counteracting large private spending shortages during periods of economic depression, or as a way of reducing the intensity of business cycles driven by the fluctuation of commodity prices in natural resource-dependent emerging market economies[3]

There is a growing consensus that the large increase observed in developed countries’ public debt is due to a spending bias of politicians which distorts democratic budgetary decision making[4] . Under these (and other) circumstances, fiscal rules can act as important anchors for long-run fiscal sustainability. Hence, fiscal rules typically aim to correct distorted incentives and contain pressures to overspend against current government revenues to ensure fiscal responsibility and debt sustainability.

Impact of Fiscal Rules on Capital Flows and Borrowing Costs

An important ongoing research question deals with the effect of fiscal rules on overall macroeconomic stability[5]. A relevant question deals with the effect of fiscal rules on sovereign default risk. If fiscal rules are useful in stabilizing government budget deficits, then they should contribute to the reduction of sovereign default risk. Paradoxically, the literature on sovereign risk has largely ignored the role of fiscal rules. Similarly, the sudden stops literature, closely related to the sovereign risk literature, has also ignored the potentially beneficial effect of fiscal rules adoption on the probability of occurrence of a sudden stop in international capital flows into a given country.

We fill this gap by studying the effect of fiscal rules implementation on both sovereign risk and the probability of a sudden capital flow reversal. Our results show that implementing fiscal rules is an effective way of enhancing fiscal and macroeconomic stability.

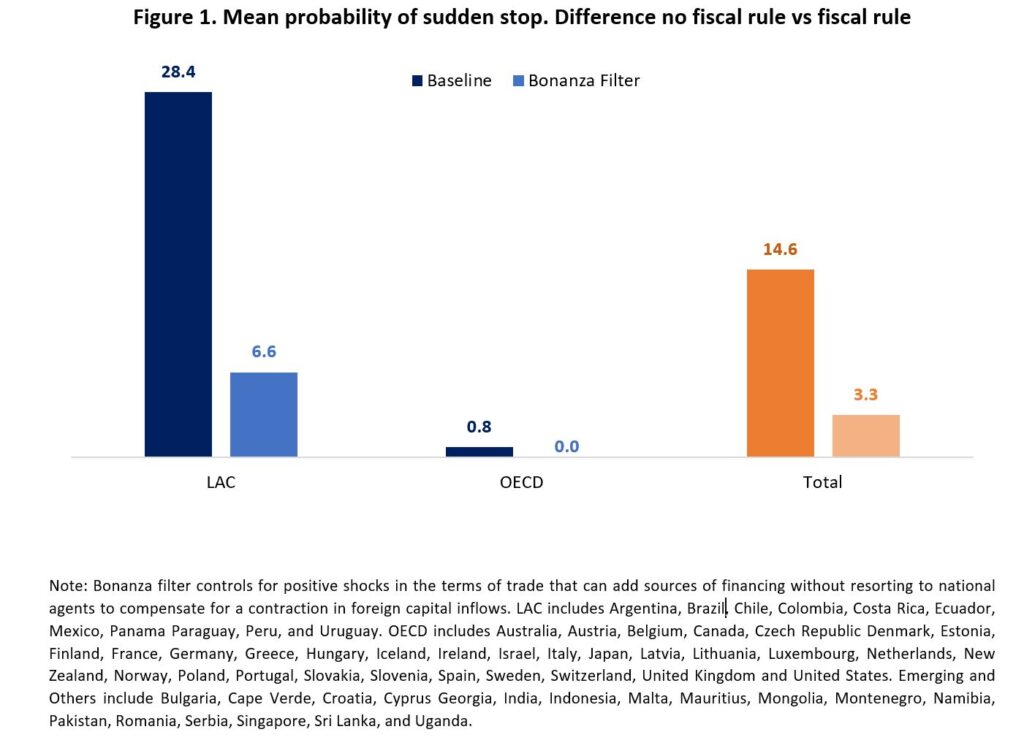

As shown in Figure 1, on average, implementing a fiscal rule reduces the probability of a sudden stop by about 14 percentage points. This effect is larger than in LAC emerging market economies, in which this probability is reduced by 28 percentage points, than in OECD’s economies where it is 0.8 percentage points.

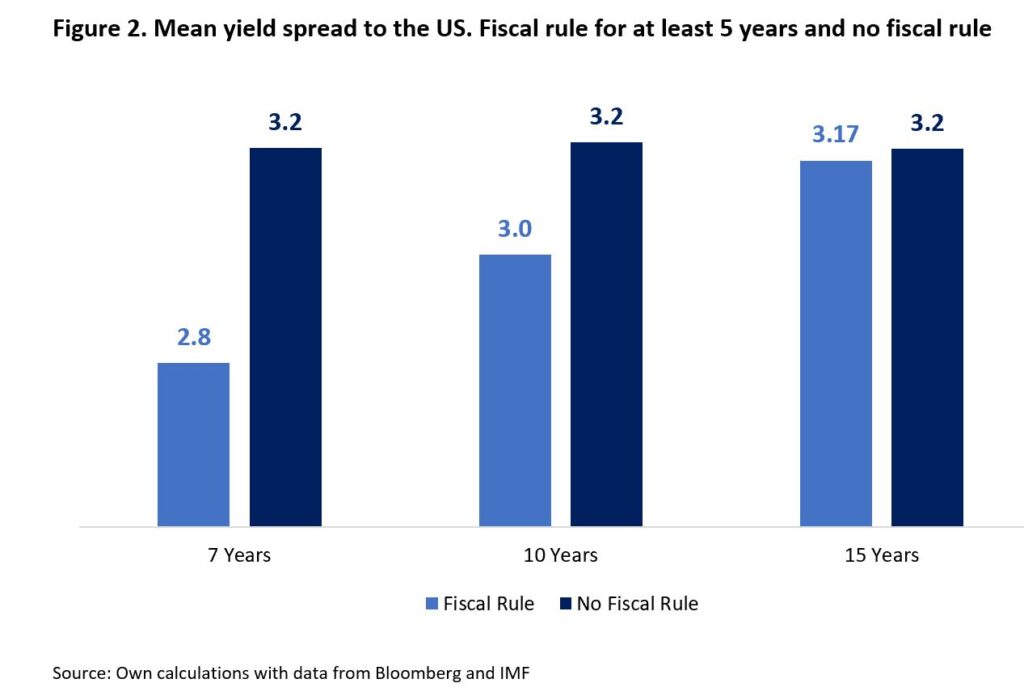

Additionally, adopting a fiscal rule reduces investors’ perception of sovereign risk, reducing the interest rate spread that countries must pay when issuing sovereign bonds in international capital markets. On average, adopting a fiscal rule reduces in 36 basis points the yield gap between a country’s ten-year sovereign bond and a U.S. treasury bill of the same maturity. As shown in Figure 2, yield spreads fall after fiscal rules are implemented in most countries in our sample.

Implementing Fiscal Rules Pays Off (Handsomely)

During the Covid-19 pandemic many countries have relaxed their fiscal rules to attend the social and economic crises through fiscal expenditure expansion. Countries are providing exceptional support to families and firms while suffering significant losses in public revenues. Debt ratios are rising, increasing the need for future debt funding. If countries want to continue to access capital markets to fund their spending at reasonable costs, they will need to provide assurances to investors that they will manage their finances responsibly.

The results of our study show that fiscal rules can provide tangible benefits for countries in terms of lower borrowing costs and greater capital flow stability, which are key pillars for ensuring macroeconomic stability, a pre-condition for any successful economic recovery plan.

As a result, countries that had fiscal rules in place should return to implementing them again and, for nations still lacking them, they should seriously consider putting them in place. The implementation of such rules will need to be adapted to the new macroeconomic conditions that will prevail in the new normal.

Uncertainty on the pandemic’s ending and on its macroeconomic effects is still high. However, it should not limit the governments’ commitment to design and maintain rules for the implementation of healthy, consistent fiscal policies that are required for a sustained economic recovery. This is an urgent task for all governments, especially those in Latin America and the Caribbean.

References

[1] Includes: Antigua and Barbuda, Argentina, Bahamas, Barbados, Belize, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Ecuador, El Salvador, Guatemala, Guyana, Haiti, Honduras, Jamaica, Mexico, Nicaragua, Panama Paraguay, Peru, Trinidad and Tobago, and Uruguay. On average, 3.9 percent in liquidity support, 3.1 percent in additional spending and 1.0 percent of GDP in deferred revenue.

[3] See Pieschacon (2012), Fernandez et al. (2018).

[5] IMF (2018) ; Cordes et al. (2015) ; Lledó et al. (2017).

This research supports the need for stringent fiscal rules in the award of IDB projects awarded to Governments and private individuals. The research has identified gaps within the funding process and proffers the theory that Covid 19 has impacted the economies of the Caribbean and central America, however the research has not identified the long term impact of impropriety in borrowing nor is the research clear on the punitive measures taken when fiscal rules are not followed.. The research has not shown with evidence the overall stewardship the bank has on corrupt officials and the wide disparity between those with control over design operations who distribute the resources to their friends and networks of public officials.

Great work on the new normal.