Following the Covid-19 pandemic, countries have been left with unprecedented rising debt levels, higher interest rates and diminished growth projections. Even though public funds are constrained, countries have agreed to ambitious targets to protect and conserve 30% of marine and terrestrial ecosystems in the Kunming-Montreal Global Biodiversity Framework as well as continue to fulfill their commitments under the Paris Agreement. Given the increasing needs for environmental finance and the sizable financing gaps identified to meet these needs, it is difficult to imagine a successful strategy to fight climate change and biodiversity loss without debt-neutral financing strategies.

To this end, debt-for-nature conversions have gained prominence as one of these strategies. DFNC are structures directed to substitute outstanding debt for new debt that is less expensive due to credit enhancement provided by multilateral development banks, development agencies or non-governmental organisations. This creates savings that are fully or partially targeted to conservation activities through conservation trust funds. These are independent, public or private organisations designed to guarantee robust execution and monitoring for long periods of time. Governance is key in DFNC as it has the intention to transform conservation commitments into financial commitments through a system of penalties and incentives embedded in the contractual structure.

MDB instruments serve as multifaceted catalysts for governance enhancement. The Inter-American Development Bank has employed a range of financing instruments, primarily policy-based with policy conditions that can require countries to meet conditions around sound debt management, conservation and climate policy, trust fund management and other enabling conditions for the achievement of conservation and sustainable debt outcomes.

The IDB has played a critical role in the negotiation of conservation commitments. Through technical assistance and advisory support, the IDB acts as facilitator between ministries of economy, environment and other authorities, conservation organisations, trust fund representatives and co-financers to design ambitious commitments in line with nationally determined contributions and national biodiversity strategy targets. The bank has also supported the development of the governance documents of the conservation trust funds, ensuring alignment with global best practice and monitoring and reporting systems. Finally, IDB has supported countries with capacity building, analytical reports and community engagement.

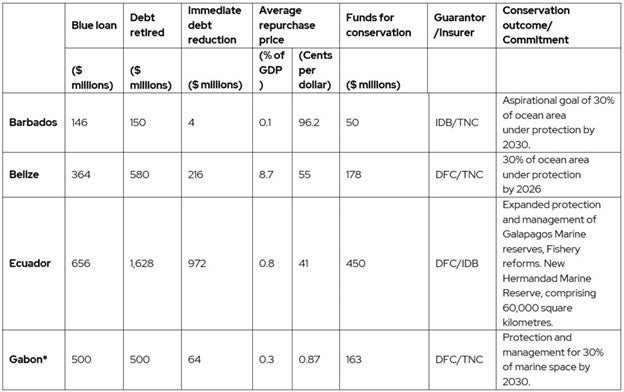

The resource mobilisation potential of this type of transaction is quite substantial. In 2023, the IDB and the US International Development Finance Corporation supported the largest ever DFNC to protect the Hermandad Marine Reserve in the Galapagos. The combination of the political risk insurance of DFC of $656m and the IDB guarantee of $85m allowed Ecuador to buy back $1.6bn, generating more than $450m for conservation over a period 18 years. Similar transactions have been implemented recently in Barbados by IDB and the Nature Conservancy with important results in terms of savings for conservation. It is worth noting that these types of DFNC represent an evolution of the first generation of debt swaps done in the 1980s, that consisted of debt forgiveness in exchange of conservation commitments.

Figure 1. Main results of recent debt-for-nature conversions

Source: Inter-American Development Bank

The version of DFNC supported by the IDB is instead based on market debt and credit enhancements, not bilateral forgiveness. These ‘new’ DFNC have mobilised more than five times more resources in only four transactions (Ecuador, Barbados, Gabon, Belize) in the last three years than over 100 efforts during the last 35 years under the past model. Notwithstanding, both models are still highly compatible and complementary in many ways.

MDBs will continue to play a catalytic role to scale up this type of transaction in the years to come. As recent experience has shown, MDBs have unique financial capacity and policy instruments to facilitate DFNC. First, most MDBs can achieve maximum levels of credit enhancement, be excellent partners for other potential co-guarantors and facilitate DFNC strategies in a wide variety of debt market situations. Second, MDBs provide a unique set of instruments for policy support and can provide technical assistance. But more importantly, MDBs are specially placed to facilitate public policy dialogue, as an honest broker, which is instrumental to reach long-term commitments between different parties (ministries, NGOs, investment banks, different types of guarantors and others).

Finally, it is crucial to underscore that MDBs alone cannot implement DFNC at the scale required to achieve the commitments assumed by governments. The presence of robust political leadership and commitment to long-term finance for conservation by countries is a necessary condition. Without the clear determination of political leaders to see natural capital as a strategic asset, there is no way forward.

MDBs must work with conservation organisations on the ground to support countries in designing and implementing conservation programmes. With the right partnerships, these transactions can not only maximise the value of MDB balance sheets, but they can also support the triple bottom line of economic, environmental and social benefits.

This blog entry, originally published on OMFIF’s website (Journal_Autumn23_IIADB – OMFIF), has been replicated on the IDB’s blog.

Leave a Reply