Fiscal rules have become a common policy tool to promote the sustainability of public finances, as the number of countries with at least one fiscal rule has grown from ten in 1991 to more than 100 by 2021. Although fiscal rules promise to support fiscal discipline and maintain debt sustainability, their track record is often mixed, as simply adopting a fiscal rule does not necessarily guarantee improved fiscal performance.

To achieve the expected impact, compliance with the rules is critical. The experience with the implementation of fiscal rules in Latin America and the Caribbean (LAC) shows that compliance with fiscal rules is far from perfect, and understanding the multiple factors that influence compliance is key to enhance the effectiveness of this instrument to promote the sustainability of public finances.

In a new working paper, we investigate the drivers of compliance with fiscal rules in the region and assess the role of rule design, macroeconomic characteristics, and political-institutional variables that influence the likelihood of compliance. Below, we summarize the main findings of the study.

Measuring Variation in Compliance with Fiscal Rules and its Consequences

The measurement of compliance draws upon an original dataset built by the IDB. This dataset captures compliance with fiscal rules in fourteen Latin American and Caribbean (LAC) countries over the last twenty years. Numerical compliance is assessed by contrasting the objectives or targets set by fiscal rules with the executed or observed values. This contrast is conducted on a country-specific basis, involving a detailed examination of legislation containing fiscal rules’ parameters and their comparison with actual fiscal performance.

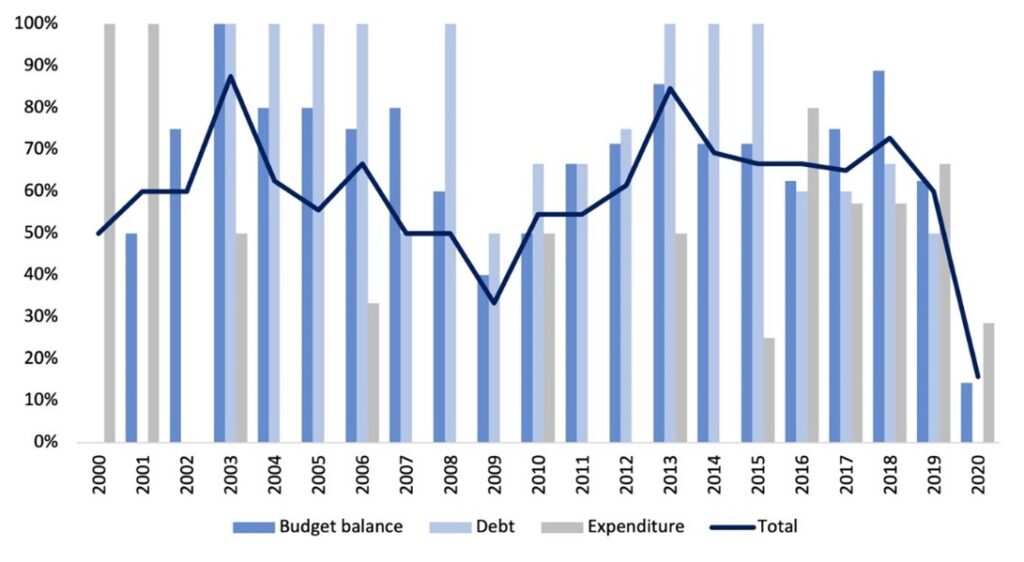

Figure 1: Compliance Rates with Fiscal Rules in Latin America and the Caribbean

Figure 1 shows variation in compliance rates across the region, showcasing changes in compliance with different rules and over time. While the average compliance rate stood at 60% between 2000 and 2020, it is noteworthy that compliance has exhibited considerable fluctuations. Compliance rates have ranged from periods of exceeding 80% to periods where they dropped below 20% on average.

These differences have clear implications for fiscal performance: periods of compliance are associated with less frequent debt acceleration episodes, lower sovereign bond spreads, and higher credit ratings. In contrast, simply adopting fiscal rules but not complying with them does not translate into better outcomes.

Four Key Compliance Drivers

Since complying with fiscal rules can significantly influence fiscal performance, it’s essential to understand which factors contribute to positive compliance outcomes. Previous research has identified several key drivers influencing fiscal policy decisions and compliance with fiscal rules: macroeconomic conditions, political-institutional variables, and design features of rules-based fiscal frameworks.

What are the main findings on the role of each of these factors in promoting or inhibiting compliance in Latin America and the Caribbean?

Macroeconomic Conditions: Compliance in Good vs. Bad Times

We find an asymmetrical response of compliance to macroeconomic conditions. While compliance decreases during bad times, it does not improve during good times.When countries experience modest GDP reductions, typically around 1% or less, they tend to adhere to fiscal rules with a strong probability, ranging between 69% and 72%. However, when GDP shocks become more severe, involving negative growth rates exceeding 10%, the likelihood of compliance drops significantly, often falling to 30% or even lower. This outcome highlights how sensitive fiscal rule adherence is to fluctuations in the economy.

Policymakers’ Forecasts: Optimistic Biases Discourage Compliance

Optimistic macroeconomic forecasts undermine compliance during the budget cycle: the probability of complying ex-post with the fiscal rule is lower when policymakers overestimate GDP growth ex-ante. Compliance with fiscal rules tends to be at its peak when fiscal authorities underestimate economic growth.

Conversely, when authorities overestimate future economic performance, resulting in positive forecast errors, adherence to fiscal rules is compromised. This phenomenon emerges from the correlation between positive forecast errors and the overestimation of fiscal balances, tax revenue-to-GDP ratios, and the underestimation of expenditures.

Institutional Quality: Strong Institutions Support Compliance

We find that a broad measure of institutional quality encompassing perceptions of the quality of policy formulation, implementation, and the credibility of government commitment to policies is a strong predictor of compliance. The results highlight a notable disparity, with countries characterized by strong institutions showing a probability of compliance that is twice as high as in countries with weak institutions.

Design Features: The Role of Fiscal Councils

Results show that specific rule design features such as introducing a formal sanctions procedures do not play a significant role in fiscal rule compliance. Interestingly, the presence of a fiscal council in charge of monitoring fiscal rules and/or targets does not seem to increase the probability of compliance either.

This result contrasts with findings from other regions, especially OECD countries, where it has been shown that fiscal councils effectively reduce compliance gaps. This finding could be partly attributed to the relative novelty of fiscal councils in the region as well as the fact that resources and technical capacity are often not proportional to the formal tasks assigned to fiscal councils, limiting their effectiveness.

Recommendations to Strengthen the Effectiveness of Fiscal Rules

Complying with fiscal rules makes a difference to a country’s credit reputation by demonstrating a credible commitment to fiscal responsibility. This increased credibility is reflected in lower sovereign bond spreads, higher credit ratings and a lower probability of public debt accelerations compared to countries that do not comply with their rules.

Despite these compliance benefits, fiscal rules do not operate in a vacuum. Instead, the broader macroeconomic and political-institutional environment affects compliance with fiscal rules. These findings have important policy implications.

First, they suggest that countries should take steps to increase commitment to fiscal rules by strengthening the role of fiscal councils during the budget process. Improving the set of tools, resources, and personnel available to councils would enhance their role in the fiscal policymaking process.

Second, the results suggest that improving budget forecasts to avoid over-optimism biases would facilitate compliance with fiscal rules early in the budget process and could go a long way toward strengthening the credibility of governments’ medium-term fiscal frameworks and fiscal plans.

Finally, strong political commitment to fiscal rules is necessary, as without such support, efforts to increase oversight and formal sanctions may prove insufficient to ensure effective compliance with fiscal rules.

Leave a Reply